This article will take approximately 29 minutes to read. Don't have the time right now? No worries. Email the ad-free version of the article to yourself and read it later!

Road accidents happen regularly in the Land of Smiles.

Thankfully, there are various choices of car insurance in Thailand from a dozen insurance companies. But the way it works can be different from the West.

This article will guide you through everything you need to know about buying car insurance in Thailand. It covers insurance options, coverage types, insurance companies, claiming procedures, and tips on choosing the right policy.

Please note that this article is primarily for those who want to buy car insurance for their cars in Thailand. If you are here for traveling and looking for car insurance for your rental car, you can check out our article on travel insurance in Thailand.

Contents

Insurance Options

There are two options of car insurance in Thailand: Compulsory Third-Party Liability Insurance and Private Insurance.

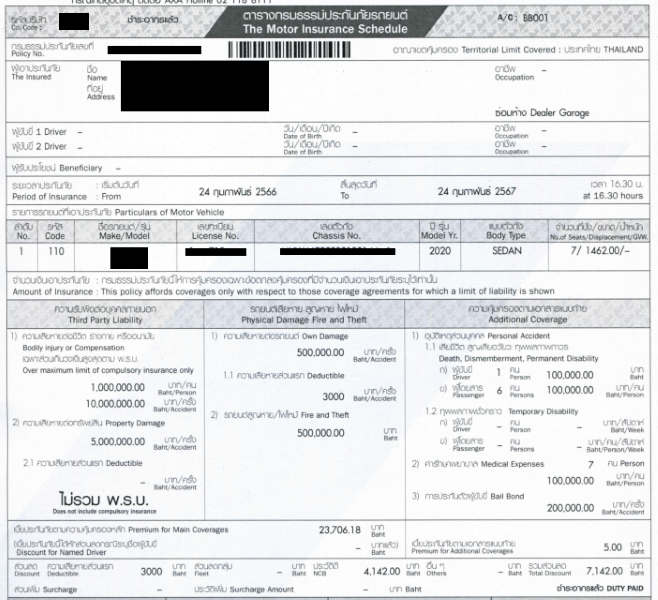

- Compulsory Third-Party Liability Insurance, known as Por Ror Bor, is required for all cars and motorcycles registered in Thailand. It needs to be renewed annually and provides basic coverage on death and injury caused from road accidents. Por Ror Bor doesn’t come with any coverage on the vehicle.

- Private insurance provides extra coverage for vehicles, medical expenses, death, and injuries. You can also get professional help when accidents occur.

Compulsory Third-Party Liability Insurance (Por Ror Bor)

Compulsory Third-Party Liability Insurance is basic insurance that all cars are legally required to get every year under the Road Protection Act. In Thailand, Compulsory Third-Party Liability Insurance is always called Por Ror Bor in short.

Coverage

Being the minimum requirement, Por Ror Bor covers only the medical expenses from a car accident per person.

The coverage of Por Ror Bor can be divided into two parts:

First, everyone can claim up to 30,000 baht for injuries and 35,000 baht for death and dismemberment.

However, if you are not the cause of the accident, the coverage will increase as follows:

- Injuries: 80,000 baht

- Death and dismemberment: 200,000 to 500,000 baht

- Daily allowance for hospitalization: 200 baht per day, up to a maximum of 20 days.

Cost

Por Ror Bor is very cheap. For a normal car, it costs only around 650 baht per year.

Do You Need It?

Yes, you need it. It’s required by law. Also, you can’t pay your annual car tax without Por Ror Bor.

Once you get Por Ror Bor and pay tax, you’ll get a sticker that needs to be put on the front mirror of your car to let traffic police see it easily.

How to Get It

You can purchase Por Ror Bor from any private insurance company in Thailand. Normally, you get it around the same time you buy private insurance.

Alternatively, you can buy it from a garage where your car is inspected for the annual tax. You can also obtain it from the Department of Land Transport.

How to Claim Por Ror Bor

When injuries happen from accidents, you can claim directly at the hospital by informing the cashiers.

Otherwise, it can be later reimbursed at the insurance company with the receipt of the medical expense, a copy of your passport, and a copy of the insurance policy.

To obtain the maximum coverage, a copy of the report from the policemen is required to prove that you did not cause the accident.

Read more: What Is Por Ror Bor in Thailand and How to Make a Claim?

Private Insurance

Private car insurance provides far better coverage than CTPL. It’s also called voluntarily car insurance.

Private car insurance in Thailand can be categorized into five types using the numbers 1, 2+, 2, 3+ and 3.

Type 1 insurance is the most expensive type providing the best coverage, covering everything from accidents, theft, and third party property damage and is mainly available for the new car only.

Type 3 insurance is the cheapest choice but only covers third-party liability and injuries.

Private Insurance Types

There are a number of insurance types you can get for your vehicle. Below is a detailed outline of each type. It’s common for people to buy car insurance from brokers in Thailand.

In my case, I always us CheckDi. It’s a comparison website developed by a brokerage company in Thailand. With it, you can compare most private insurance plans on their website and buy car insurance from them directly. The price is also cheaper than what I found from other brokers.

Type 1

Type 1 is the most expensive and comprehensive type of insurance offered in Thailand. Some may call it first class insurance. It should cover you from all accidents and problems.

Also, it’s the only insurance type that covers an accident not involving a third party, such as hitting a wall, hitting a dog, getting a scratch, and so on. Type 1 insurance also have the highest amount of overall coverage limit.

You can get the Type 1 insurance if your vehicle is less than 7 years old. Alternatively, if you have an older car, it is still possible to get it as long as it has a good record and history without major accidents involved.

Type 2+

Type 2+ is the second most expensive car insurance option in Thailand. Its coverage is similar to Type 1 insurance but does not cover accidents where no third party was involved.

In addition, Type 1 insurance tends to send your car for repairs at official garages while type 2+ insurance will be sent to 3rd party independent garages instead.

Also, the coverage limit for Type 2+ is normally much lower than that of Type 1 insurance.

Type 2

Type 2 insurance is similar to Type 2+, including price, but doesn’t have collision coverage.

Because of this, a majority of people prefer Type 2+ over Type 2 insurance. And only a few insurance companies are now offering it.

Type 3+

Type 3+ insurance comes with necessary road accident protection, collision coverage, and third party property damage.

The main difference between 2+ and 3+ is that Type 3+ does not have theft, fire, flood, and terrorism protection. The overall coverage limit is even lower.

In my opinion, Type 3+ car insurance is great if you have an older car and still want the insurance company to cover the cost of repairs in case of an accident.

Type 3

This is basic private insurance and covers only medical expenses and third-party liability. This means that if you have a car accident, the insurance will not cover the cost of repairing your car.

It is popular for old or low-valued cars for many Thais.

Coverage

- One-party Accidents: Only Type 1 insurance covers accidents that happen without a third party involved. This includes hitting a wall or dog, scratching a structure, crashing into a tree, and so on. However, you may need to pay an excess fee of at least 1,000 baht. The fee differs based on your insurance plan.

- Collision: Type 1, 2+, and 3+ insurance normally comes with collision coverage. It covers the cost of repairing your car as long as it is caused by hitting another car. Pay attention to small details on the collision coverage policy since expensive plans allow you to have your car repaired at the official garage of your car’s brand, while cheaper plans send you to individual garages. If you caused the accident, an excess fee might be required. If the collision damage is beyond repair, you may receive 70%-100% of the insurance limit in return.

- Medical Expenses: All insurance types include medical expenses caused by car accidents. The coverage amount is likely to be similar, no matter what insurance types you are using. And it is lower if you cause the accident. Insurance companies require a medical receipt for reimbursement unless you go to their partner hospital. You can use car insurance, health insurance, and family insurance to cover your medical expenses.

- Theft: You may not be under theft protection coverage if your car is stolen because of your own carelessness, including forgetting to lock it, parking it in an unsafe place, or embezzling it. You may only receive 70-80% of the insurance limit based on your vehicle’s age.

- Fire/Flood: Similar to theft protection, you can claim from flood damage only when it’s not your fault. If you park a car and that area suddenly becomes flooded, you are under the coverage. On the other hand, if you intentionally drive through flooded areas, insurers may reject your claim. This type of coverage always comes with Type 1 insurance and some Type 2 or 2+ insurance only.

- 3rd Party Property Damage: The whole idea of the 3rd Party Property Damage is similar to collision coverage but only covers the car of the opposing party. This is the selling point of Type 3 coverage because you’ll only need to fix your own car from the accident without having to worry about the opposing party.

- 3rd Party Personal Injury: All types of insurance, including Compulsory Third-Party Liability Insurance, or CTPL, come with 3rd Party Personal Injury coverage as long as it is caused by a car accident. It means that if you get hit by a car while walking down the street, you can at least get reimbursed from CTPL in addition to asking the driver for compensation.

Coverage Limit

There is a coverage limit for all car insurance policies.

Type 1 insurance typically covers around 70 – 80% of your current car’s value when it comes to the limit for repairing your car or in the event of fire and theft.

For other types of insurance, this limit tends to be much lower.

When it comes to medical expenses, the coverage is usually around 100,000 baht per person. This is usually sufficient for a minor accident.

However, in the case of hospitalization, unless you have health insurance, you may need to pay out of pocket.

Regarding third-party liability, private insurance for all types normally covers around 1,000,000 baht for death and dismemberment, and 5,000,000 baht for property damage.

Please note that the coverage limit can vary between insurers and plans. Therefore, it’s important to read the fine print.

Additional Benefit

There is an additional benefit of having private car insurance. Even the cheapest package has hidden cons providing you peace of mind while driving as follows:

- Helping with Argument: When a car accident happens, it’s a common case in which drivers–and maybe motorcycle taxis around–blame one another, trying to find the guilty side so they won’t have to pay for the damage caused by an accident. With car insurance, insurance reps will argue for you and try to win the conversation because they don’t want to lose money as well.

- Prevent Overcharged Repair Price: Without car insurance, the third party may take this opportunity to overcharge the cost of repairing a vehicle. The price can double from 50,000 baht to 100,000 baht. Worse, you may even need to go to court if you disagree to pay.

- Road Assistant: Since a car insurance rep needs to regularly deal with road accidents, they have contact details in hand and help you solve the situation from calling a towing truck, talking to traffic police, and dealing with opposing parties.

Coverage Comparison and Price

Below is a table comparing the normal coverage and prices for all insurance types. It should give you a rough idea of how much you’ll pay and what should be covered.

Please note that coverage varies based on several factors, including the age of your car, your car’s price, the insurance company you choose, and so on.

There are also other factors, such as if the insurance company sends the car to an official garage for repairs, the insurance package will cost more than if it is sent to an independent garage.

Some offer deductibles–often confused with an excess–making the insurance plan lower. But you need to pay for the fixed fee when making claims. There are also no-claim bonuses, pay-per-use insurance, and driver specification choices.

| Coverage Type | 1 | 2+ | 2 | 3+ | 3 | CTPL |

| Self Accident | O | X | X | X | X | X |

| Collision | O | O | X | O | X | X |

| Medical Expenses | O | O | O | O | O | O |

| Theft | O | O | O | X | X | X |

| Fire/Flood | O | O | O | X | X | X |

| Terrorism | O | O | O | X | X | X |

| 3rd Party Property Damage | O | O | O | O | O | X |

| 3rd Party Personal Injury | O | O | O | O | O | O |

| Avg. Annual Price | ฿20,000 | ฿7,000 | N/A | ฿5,500 | ฿3,000 | ฿650 |

Understanding Excess

Excess is mainly for Type 1 insurance in cases of self-accidents.

You need to pay an excess when damage or scratches occur without a clear cause or when no third party is involved. This includes scenarios such as a nail piercing a tire while driving, a windshield breaking suddenly for no apparent reason, parts damaged by animals, unknown scratches, and so on.

On the other hand, if you can report an accident, including hitting a wall, poles, trees, animals, or stones, you don’t need to pay excess.

If the damage is caused by another car, the excess can still be waived if you were not at fault for the accident. Excess usually starts at 1,000 baht per incident of damage.

However, each insurance company has a different policy regarding excess.

Even some insurance representatives might give you incorrect information. It’s important to read the fine print in detail and recheck everything if you are unsure whether the excess can be waived or not.

Exclusions

Below are standard exclusions which every car insurance company can reject your claims for: not having a driver’s license, drunk driving, unauthorized driver, using your car as a taxi or moving vehicle, leaving the scene of an accident, and wars.

The exclusion may be different between each insurer. Be sure to read the fine print carefully.

- Driver’s License: Insurers do not cover drivers if the driver does not have a driver’s license.

- Drunk Driving: According to Thai law, a person who has blood alcohol concentration, or BAC, of more than 50mg is considered drunk. It does not only result in the denial of insurance claims, but there’s also a chance of getting fined and imprisoned.

- Unauthorized Driver: This is different based on the insurance package. Some packages might cover every driver as long as he/she has a license and isn’t drunk, while some only cover a specific person who can drive the car.

- Incorrect Purpose: Some insurance companies might not cover you if you use a car in an unsafe manner. This includes carrying more passengers than the vehicle should carry, using a personal car to transport goods or move, and installing NGV or LPG gas systems without giving notification.

- Leaving the Scene of an Accident: If you cause the accident and leave the scene, the insurance company does not cover costs. This is considered a crime in Thailand and will result in court.

- War: Car insurance companies might reject claims caused by war and protest, no matter if you are living in a risk area or not. If the damaged is caused by these events, you are not under coverage.

Insurance Company

The car insurance market in Thailand is pretty big.

There are essentially over twenty car insurance companies in Thailand.

Two of the most famous car insurance companies in the local market are Viriyah and Bangkok Insurance. Despite being more expensive than other insurances, they have the highest number of partner garages and are known for easy claim procedures and support.

Other major players in this industry are Dhipaya, Deves, Allianz, Muang Thai, Roojai, and Tokio Marine. These insurance companies still have their own representatives and partner garages all over the country.

In addition, many banks such as Thanachart, SCB, Kasikorn, Krungsri, and TMB have recently launched their own car insurance. The main targeted customers from these financial institutions are those who make a financial car loan with them.

You can find out more in our exclusive article on how to choose the right car insurance company.

Finding the Best Car Insurance

Since each car insurance company has their pros and cons, it is hard to indicate which one is the best car insurance company out there.

From what we gather, people have different experiences even with the same insurance provider.

Instead of finding out the best insurance, it is better to choose a credible company with a plan that is most suitable for you.

Here are a few things you should consider:

- Reputation: Apply with an insurance company that has been in this industry for a long time. With insurance companies you never heard of before, it is better to check their financial background.

- Staff Knowledge and Service: Since you need to deal with the insurance company’s staff in the long run, find out in advance whether they can provide satisfactory service or not. You can check this by calling them and explaining your needs. If the staff just redirect your call without providing professional service, just ignore them and choose a new company.

- Additional Features: Because of the competitiveness of this industry, insurance companies have been regularly introducing new features and services. This ranges from providing a substitute vehicle or compensation when your car is under repair to a discount for loyal customers.

- Nearby Garage: Dealing with a garage that’s not a partner with the insurance company is quite complicated. Therefore, you can talk with a reputable garage near you and ask which insurance company they partner with. This way you will know in advance where to repair if an accident happens.

In Thailand, people tend to purchase car insurance from insurance brokers. The price you get from them can even be cheaper than buying from insurance companies directly.

Because of the competitiveness in this industry, some brokers also provide additional benefits to their customers.

The common benefits include helping with the buying process to dealing with claims. Some even offer a loaner car when your car is under maintenance.

In the past, brokers were recommended by word of mouth and friends.

But everything now is online. There are various insurance broker websites providing both insurance comparison services and allowing you to buy the insurance at the same time.

The one we recommend is CheckDi, which is previously known as Mister Prakan. The website is functional, easy to use, and has English speaking customer support with an online form to find out the cheapest and most suitable plan based on your needs.

Buying Procedure

When you buy car insurance in Thailand, it can be done online.

The process is going to be like this:

- After you choose a plan, you will talk with a broker or insurance representative and send the following documents:

- A copy of the car’s registration.

- A copy of the first page of your passport.

- A copy of your driver’s license.

- A copy of your previous insurance policy, which might be required.

- Pictures of your car (Type 1 insurance only), including the front, back, left, and right sides, are required. Some insurance companies might even send their agents to inspect your car directly. This is mostly on a case-by-case basis.

- Transfer the payment via a credit card or a wire transfer

- Wait for the insurance policy to be sent to you, either to your email or address.

Decreasing Car Insurance Premiums

There are many things you can do to decrease your car insurance premium.

Deductible

Deductibles can significantly reduce the cost of car insurance.

A deductible is a fixed amount you agree to with the insurer when you want to make a claim. If the deductible amount is 3,000 baht, it means that you need to pay an additional 3,000 baht whenever you make a claim, on top of any excess fee.

For example, with a 3,000 baht deductible, the cost of Type 1 insurance plans that are normally 15,000 baht a year might decrease to only 11,500 baht.

You don’t need to pay a deductible if you are not at fault in an accident. So, it’s a good option if you believe in your driving skills.

Typically, the deductible amount ranges from 1,000 to 5,000 baht. Similar to an excess, its amount and policy is different between each insurance company.

Important: Note that excess and deductible is commonly misused in Thailand, even with insurance representatives. They share the same word in Thai. So carefully read the fine print.

No-Claim Bonus

Many insurance companies in Thailand offer no-claim bonuses, giving discounts on renewal rates for those who have not made any claims, or who’ve made only a few small claims, in that year. This is only available with some insurance plans, mostly on the Type 1 insurance.

On the other hand, the renewal rate will be increased if claims are made within the same year.

Official and Individual Garage

When choosing car insurance, especially for Type 1, 2+, and 3+, you will be asked whether you want to have your car repaired at an official garage or individual garage.

Official Garage

The official garage is the garage from your car’s manufacturer. For example, if your car is Toyota, it will be sent to an official Toyota garage for repair.

Pros of the official garage are that your car will be repaired by certified car mechanics using genuine replacement parts. The garage may replace a new part instead of fixing the old part. This results in the car having no problems after repair.

?

? - A lesson structure to help you effectively learn Thai

- Thousands of Thai language lessons with lesson notes, podcasts, and quizzes

- Learn Thai on the go through their mobile application

- Personalized program to learn exactly on what you need

- Affordable price starting at only $8 a month

- 60-day moneyback guarantee

However, repairing at the official garage tends to take a lot of time because of long queues.

Garage locations, especially in the countryside provinces, are also quite limited, and the insurance package is more expensive.

Individual Garage

There are a lot more individual garages than official garages. They are easier to find, faster, and cheaper. However, you need to carefully pick the garage. It is common to hear stories from people sending their cars to the individual garage resulting in more problems.

Some individual garages may use fake parts and carelessly fix your car causing more problems in the future. It is also common to hear that paint jobs by individual garages do not match the original car color.

There are, of course, individual garages with good standards. But this would require further research.

It is also different when making a claim on an individual garage who is a partner with the insurance company and who is not. You can find out more in the claiming procedure section below.

Driver Specification

Car insurance prices depend primarily based on your driving history. If you have a good record, your premium will be lower.

Since August 2025, discounts have been decided under a two-factor system based on driving history and claims, with five levels in each category.

For driving history, maintaining a good driving record each year earns an additional 10% discount. Drivers start at Level 1 with no discount at the beginning of their insurance policy. From the second year onward, a 10% discount applies, increasing annually up to a maximum of 40% in the fifth year.

The driving-history discount is combined with a no-claim bonus. If no claims are made, an additional 10% discount is added each year. As a result, the maximum total discount available on an insurance premium is 80%

The discount is only given on the premium price, not the excess fees.

Pay Per Use

Thaivivat introduced a new pay-per-use insurance option. The idea is similar to a prepaid cell phone package. The vehicle will be under coverage for the amount of given hours per period.

For example, 144 hours for thirty days, 600 hours for one hundred and eight days, and 960 hours for three hundred and sixty days. The package price is lower than normal insurance plans, but you are limited to use your car for three to five hours per day on average. When running out of hours, you can top up just like you’d top up your mobile phone.

The main weakness of pay-per-use insurance is the complexity.

The prepaid Thaivivat application needs to be turned on before driving to be under coverage, and turned off after that. If driving in an area with a low internet signal, you’d have to call the insurance company notifying which time you want to drive.

Add-Ons

There are also car insurance add-ons providing extra coverage that may not be included in the insurance package.

This ranges from getting compensated for your belongings getting stolen from your car, paying for travel, receiving medical care, paying for temporary transportation, paying consolation money, or getting towed or loaner cars.

Making a Claim

As with other types of insurance, in order to file a claim with your car insurance company you have to follow certain procedures.

When Having Road Accidents

When road accidents happen, the first thing you need to do is call your insurance rep, take photos from as many angles as possible, showing your car’s license plate from both sides, and then wait.

You should not move the car unless asked by policemen or if deaths are involved.

It is the insurance rep’s duty to help you find out which party is the cause of the accident–if it is unclear. A lot of people decide to get car insurance for this specific reason because they do not want to argue with the other party when a road accident occurs.

If either party admits the fault, you can move the car to the side of the road to prevent a traffic jam. However, you still need to wait for the insurance rep.

After the insurance rep arrives at the scene and decides the at-fault party, you will receive a claim form which can be later handed into the insurance company.

The only condition that you can move the car and leave the scene right away without having to wait for the insurance rep is through the knock-for-knock agreement.

In this scenario, both parties should be under first class insurance coverage, can agree who’s fault it is, and there are no deaths. Then, they need to exchange a claim form with all information filled in and state directly which party is at fault. The claim form can be submitted later to the insurance company.

The best way to prove the fault of the opposing party is through having a dash cam. Make sure it is working properly and choose the one that can produce good quality even in low-light situations.

Submit Your Claim

In case you already have the claim form from the insurance rep, you can immediately submit it to the insurance company’s partner garage.

After submitting, you should receive a claim number for tracking purpose.

Many insurance companies offer online claims through Line.

You can give them all related information such as car details, accident details, photos, and the at-fault party. Then, the system should issue a claim number which you can later use to contact the insurance company’s partner garage.

The process of repairing a car at the insurance company’s partner garage is quite smooth and straightforward.

After submitting the claim, the partner garage will have everything taken car of and appoint you the date to get your car back.

Claim Paperwork

Here is a list of documents that are normally required for claiming.

- a copy of car registration

- a copy of the first page of a passport

- a copy of driver license

- a copy of insurance policy

- a copy of the first page of a bank account book, if there’s any compensation

Choose a Garage

If your insurance policy covers only individual garages, you need to choose a garage where you want to have your car fixed. Not all of them are good.

Feel free to visit a few garages first and choose the most credible one, or you can ask your Thai friends for a recommendation.

If any garage asks you for a deposit, check with an insurance representative first before giving them money.

You can still repair a car with the garage that is not a partner with the insurance company, but this requires additional work. The first thing you need to do is to contact the insurer and ask for the budget for repairing your car.

Each insurer has different methods to do this. Some may need you to have the car checked with them while some only require a few pictures. Also, some insurers can give you the budget a day after all information is sent, while others may take a week.

You also need to pay the repair cost yourself first, and the reimbursement will be sent around a month later. If the actual cost is higher than the insurer’s budget, you need to pay it yourself. Also, some garages might charge an additional processing fee for 1,000 baht.

It is counted as their extra work and cost to deal with the insurance company.

Going Without Car Insurance

Buying private car insurance is optional in Thailand, as having Por Ror Bor is completely legal.

In our opinion, it’s not recommended to rely solely on this. Car accidents occur frequently in Thailand, which has the 9th-worst accident rate in the world and the deadliest in Southeast Asia.

At the very least, consider getting Type 3 insurance. It costs only a few thousand baht and covers third-party liability damage. This can save you the headache of dealing with an accident and provide extra peace of mind while driving.

Where Should I Buy Car Insurance?

There are plenty of ways to buy car insurance in Thailand, but I usually use CheckDi to compare all the plans in one place. After that, I chat with one of their insurance agents to get their take based on what I’m looking for. Once I feel good about it, I go ahead and buy through them.

It’s super convenient. Plus, I’ve noticed their prices are usually a bit cheaper than other brokers.

If you are looking for motorcycle insurance, we have a separate guide to the motorcycle insurance. You should head there and find out more information about this topic.