This article will take approximately 13 minutes to read. Don't have the time right now? No worries. Email the ad-free version of the article to yourself and read it later!

Every registered company in Thailand must file withholding tax returns (PND 3 or PND 53) monthly and issue Withholding Tax Certificates to vendors. Rates run from 1% to 5% depending on service type.

In Thailand, registered companies are required to file withholding income tax returns for services purchased from individuals or juristic persons. The withholding income rate is between 1% to 5%, depending on the type of service performed.

Withholding Income Tax returns need to be filed monthly within 7 days or 15 days after the end of the month in which the assessable income is paid, with the PND 3 form being filed for individuals and PND 53 for juristic persons that service your company.

Read on to find out more about filing withholding income tax returns and how you can submit the PND 3 and PND 53 for entities that service your company in Thailand.

Contents

- Key Takeaways

- What Is It?

- Who Needs to File It?

- How to Prepare PND 3 and PND 53

- Withholding Income Tax Rate

- Supporting Documents for PND 3 and PND 53

- How to File PND 3 and PND 53

- Issuing Withholding Tax Certificates

- Can I File it Myself?

- How to Pay Tax

- How to Claim Withholding Income Tax Refunds?

- When to File Your PND 3 and PND 53

- Late Fines

- Exemption

- Now, on to You

Key Takeaways

- Every registered company in Thailand must file PND 3 (for individual vendors) or PND 53 (for juristic person vendors) each month, regardless of company size.

- The filing deadline is the 7th of each month for paper submissions, extended to the 15th when filing online through the Revenue Department e-filing portal.

- Withholding tax rates depend on the service type: 3% for most services, 1% for transportation, 2% for advertising, and 5% for rent.

- You do not need to withhold if the total payment to a vendor in a single month is under THB1,000, unless there is an ongoing contract.

- If you pay a vendor the full amount without withholding, you are liable to pay the withheld tax yourself, plus any applicable interest.

- You must issue three copies of the Withholding Tax Certificate for each transaction: copies 1 and 2 go to the vendor, copy 3 stays with your company.

- Classifying vendors correctly as individuals or juristic persons from the start prevents filing errors and amended returns later.

- An accountant who knows the Thai Revenue Department system can handle monthly filings, liaise with officers in Thai, and keep your company in compliance for a modest fee.

What Is It?

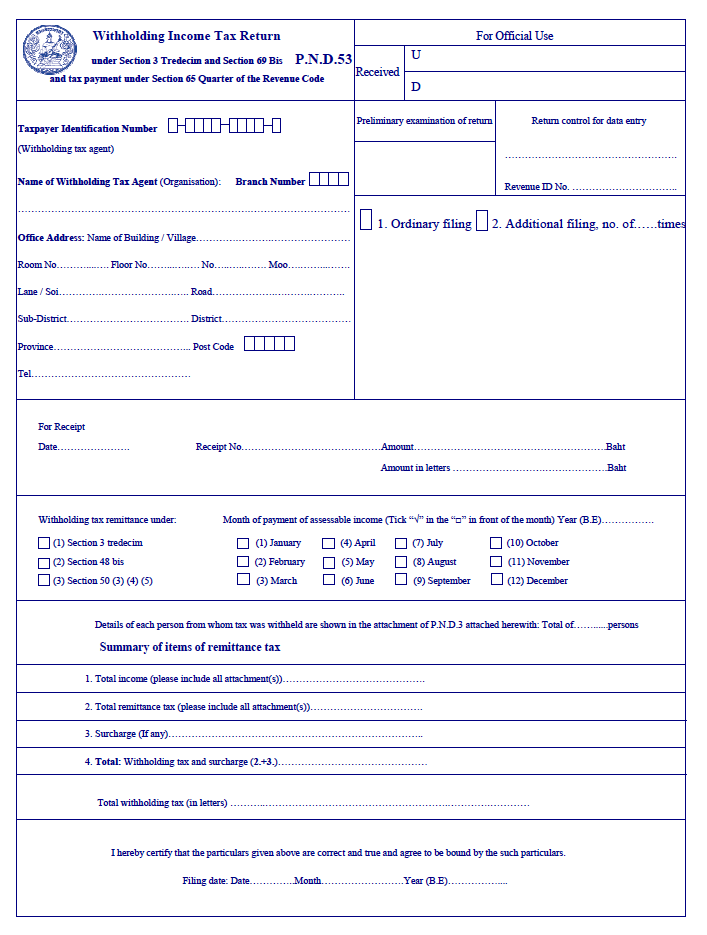

The PND 3 is the Withholding Income Tax Return form for individuals, and the PND 53 is the Withholding Income Tax Return form for companies.

The way withholding tax works in Thailand is that your company deducts the withholding tax from payments for entities that service your company. For example, if an individual translator charges you 1000 THB, you are liable to deduct 3% withholding tax (30 THB) from the payment which will be filed in the PND 3 form by the 7th or the 15th of the following month.

Your company must pay the 3% tax to the Revenue Department along with filing the PND 3, and mail or provide two copies of the Withholding Tax Certificate to the individual, who will be able to use this form to claim tax refunds for withholding tax when they file their Thai income tax return in March of the following year.

You need to file the correct form (PND 3 or PND 53), recording the filing status of the entity that serviced you – and paying the appropriate percentage of withheld tax according to the service – to the Revenue Department within 7 days or 15 days after the end of the month if you have a registered company, regardless of the size of the business.

Who Needs to File It?

Companies in Thailand must withhold the designated percentage of taxes from their vendors when making payments for different types of services.

Payments to overseas vendors are also liable for withholding tax if they meet certain criteria.

A local accountant can help you with the filing process at the end of each month.

One detail that catches many small businesses off guard: you must classify each vendor correctly as an individual or a juristic person before filing. Using PND 3 when PND 53 is required (or vice versa) results in an amended return and additional work with the Revenue Department. Building a simple vendor intake process that records tax ID and legal status from the start saves significant trouble later.

Learn More:

- General: A Step-by-Step Guide to Registering a Company in Thailand on Your Own

- Get the Right Company for Accounting Service in Bangkok, Thailand

How to Prepare PND 3 and PND 53

You can get an English copy of the PND 3 form, PND 53 form and Withholding Tax Certificate from the Revenue Department website.

Within the PND forms, you need to list out information about the amount paid for the service, month in which it was paid, and tax ID of the entity that serviced your company.

PND 3 forms are issued for payments made to vendors who are individuals, and PND 53 forms are issued for payments made to vendors who are juristic persons who serviced your company during the past month.

Withholding Income Tax Rate

Rates of withholding taxes vary according to the type of service and are taxed at a percentage of the vendor’s service fees:

- Most types of services – 3% (legal services, accounting services, repairs, cleaning, construction, etc)

- Transportation – 1%

- Advertising – 2%

- Rent – 5%

Related article: An Expat’s Guide to Finding Work in Thailand

Supporting Documents for PND 3 and PND 53

To prepare the PND 3 and PND 53 for each month, you need to send all of the following to your accountant:

- Copies of ID cards of individual vendors who serviced your company

- Company name, address and taxpayer identification number for companies that serviced your company

- Invoices from services performed for your company in the past month

After that, the accountant will fill out the PND 3 and PND 53 forms and send it to the Revenue Department, along with issuing copies of the Withholding Tax Certificate to each of the entities that serviced your company for them to file for tax refunds during their annual tax return filing.

How to File PND 3 and PND 53

There are two ways you can file the withholding tax forms. You can file it on paper at your local Revenue Department, or you can e-file it through the E-Filing website.

You just need to choose the PND 3 or PND 53 form and file it digitally.

After that, you can save the file to your company for a record. It is suggested to save your company tax documentation for a minimum of five years. For a broader overview of corporate tax obligations, see our guide to PND 50 (corporate income tax).

If your company does not yet have a username and password for e-filing, you can use this website to fill out the Por. Or. 01 request for e-filing.

If you use an accountant to open your company and register for VAT, they may have already created an account for you.

E-filing is much more convenient, and most companies have shifted to e-filing already.

Learn More:

- Taxes You Have to Deal with as a Business Owner in Thailand

- General: How Long Should You Keep Company Documents?

Issuing Withholding Tax Certificates

Once you have paid withholding income tax to the Revenue Department, your company will also need to generate three copies of the Withholding Tax Certificate for each PND 3 or PND 53.

Withholding Tax Certificates can be filled in and printed via most Thai accounting software, or a booklet of blank Withholding Tax Certificates can be purchased from local stationery stores and filled in manually for issuance to vendors.

Copies 1 & 2 are given to the vendor – one is to be attached with the income receiver’s tax return, and the other is to be kept by the income receiver as a reference. Copy 3 is to be kept by the income payer (your company) as a record.

Can I File it Myself?

Although it’s possible to do it yourself, it’s better to hire an accountant to prepare and file the monthly PND 3 or PND 53 forms and issue Withholding Tax Certificates for your company, to prevent any penalty for filing incorrect information.

The accountant can also help you talk with a Revenue Department officer when they have any questions with the form – which is really helpful unless you can speak Thai fluently.

Learn More: The Complete Guide to Learning Thai Online And Available Courses

How to Pay Tax

After you file the PND 3 and/or PND 53 forms, you can pay withholding tax directly to a local Revenue Department, make a bank transfer, or though a QR payment.

How to Claim Withholding Income Tax Refunds?

You can claim your withholding tax refund yearly along with the filing of the annual tax return through the E-filing website to recover all of your withheld income.

To do it, you must submit all Withholding Tax Certificate copies received from customers to the Revenue Department. The total amount from all Withholding Tax Certificates submitted will be issued as a tax refund.

There are three options for receiving a withholding income tax refund: it can be in cash (if they file it at a local Revenue Department), via bank transfer, or they get a tax credit for tax filing.

You can combine the withholding tax amount with your annual tax return. If the total tax owed is more than the amount of income withheld, you must pay additionally. But if the amount tax owed is less than the amount of income withheld, you can request a tax refund.

Learn More:

- Increase Your Chances of Getting Tax Refunds

- When and How to File Taxes as a Business Owner in Thailand

When to File Your PND 3 and PND 53

The following deadlines for corporate income tax filing apply to companies incorporated under Thai law:

- PND 3: Within the 7th day of each month if paper filing

- PND 53: Within the 7th day of each month if paper filing

Currently the Revenue Department provides a grace period until the 15th of each month if filing withholding tax forms online – however, this policy is only being extended on an annual basis, so make sure to check for any policy updates on filing deadlines each new fiscal year.

Late Fines

It is important to complete the Withholding Income Tax Returns on time to avoid penalties, and accurately to prevent having to file amended returns.

There are severe penalties for not filing company taxes according to schedule as follows:

- The penalty for filing each form late (or not filing at all) for the month is a fine not exceeding 2000 THB per form, along with interest of 1.5% per month on the amount of withholding tax owed. Exceptions will only be made in case of a force majeure.

- Any person who deliberately fails to submit the required forms in order to avoid paying taxes is liable to imprisonment for a term not exceeding 1 year or a fine not exceeding 200,000 THB, or both.

Additionally, because the law requires you to withhold the tax and submit it to the Revenue Department by the 7th of the following month (or the 15th if filing online), if you pay any vendors fully and fail to withhold the tax, you will have to pay the tax yourself.

A practical point worth knowing: if you pay a vendor in full without withholding, the law requires you to cover the tax yourself out of pocket. Many business owners discover this only after their first Revenue Department audit. Withholding at the time of payment is far less painful than paying it retroactively with interest.

Learn More:

- Taxation in Thailand: 6 Common Mistakes

- Get the Right Company for Accounting Service in Bangkok, Thailand

Exemption

You do not need to withhold tax if the total amount is less than THB1,000 in a single month.

For example, if you hire a freelance translator and it costs you THB999, you don’t need to withhold tax and can pay the translator in full.

However, if you need the service again that month, and need to pay the same translator another fee, then, you need to withhold tax for both payments.

However, if you have a long-term contract with that freelancer, you still need to withhold tax.

Now, on to You

Handling company accounting in Thailand – filing withholding tax returns and issuing Withholding Tax Certificates – can be complex, especially if you don’t speak Thai. Become aware of the tax returns you are liable to file as a business owner, and don’t fall prey to common accounting mistakes.

Remember that with the help of local accounting firms who know the ins and outs of the Thai accounting system and are experienced in dealing with the Thai Revenue Department, you can stay in compliance with little to no headache even without a large accounting budget.

We have exclusive business content with insider business tricks that you can’t find anywhere else.

By becoming a subscriber of our Business tier, you can get immediate access to this content:

- Karsten’s List of Personal and Professional Services

- A Step-by-Step Guide to Registering a Company in Thailand on Your Own

- Taxes You Have to Deal with as a Business Owner in Thailand

- Employee Regulations You Must Know as a Business Owner

- Increase Your Chances of Getting Tax Refunds for Your Company

That’s not all. You get a free consultation with a corporate lawyer, a free consultation with an accountant, enjoy ExpatDen ad-free, and get access to over a hundred pieces of exclusive content to make your life in Thailand hassle-free.

Here is the full list of our exclusive content.

To get access to these exclusive business guides and more, become a subscriber.