This article will take approximately 12 minutes to read. Don't have the time right now? No worries. Email the ad-free version of the article to yourself and read it later!

The PND 51 is Thailand’s half-year corporate income tax return, filed each August by all registered companies. This guide covers who must file, how to estimate profit, and how to avoid penalties that catch first-time filers off guard.

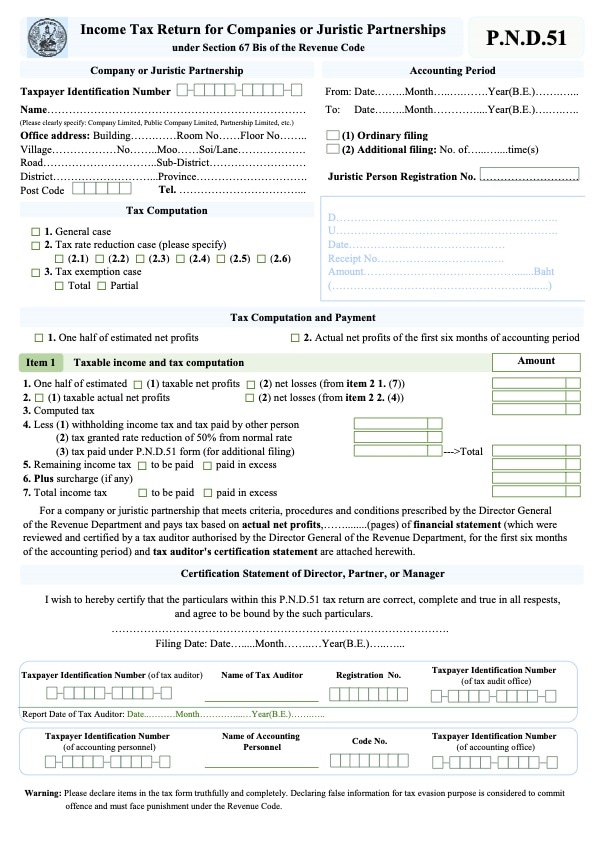

The PND 51, also referred to by some as the Half-Year Corporate Income Tax Return, is a tax return form that needs to be filed mid-year by companies and juristic partnerships in Thailand.

Read on to find out more about semiannual corporate income tax returns and how you can submit the PND 51 for your company in Thailand.

Contents

- Key Takeaways

- What Is It?

- Who Needs to File It?

- How to Prepare PND 51

- Corporate Income Tax Rate

- Supporting Documents for PND 51

- How to File PND 51

- Can I File it Myself?

- How to Pay Tax

- How to Get Tax Return

- When to File Your Half-Year Income Tax Return

- Late Fines

- Amended PND 51

- What If I Need to Close the Company?

- Now, on to You

Key Takeaways

- Every registered company in Thailand must file PND 51 each August, even if the company made a loss or holds a BOI tax exemption.

- PND 51 requires an estimate of the full-year annual profit divided by two, not a report of actual first-half results.

- If your estimated net profit falls more than 25% below your actual annual profit without a justifiable reason, you face a 20% surcharge on the unpaid tax.

- Filing mid-year tax equal to at least half of the previous year’s PND 50 tax is treated as reasonable cause by the Revenue Department, protecting you from the 20% surcharge.

- If you do underestimate, filing an amended PND 51 before the year-end PND 50 triggers only a 1.5% monthly surcharge on the difference, far less than the 20% penalty.

- E-filing through the Revenue Department’s online system gives you an 8-day extension beyond the standard August 31 deadline.

- Keep all supporting tax documents, including the filed PND 51, for a minimum of five years.

What Is It?

The PND 51 is the Half Year Income Tax Return for Companies or Juristic Partnerships. You need to file it each August to the Revenue Department if you have a registered company, regardless of the size of the business.

It is a projection of your expected revenue minus expected expenses.

Note: Corporate income tax must be paid twice per accounting period using the Half-Year Income Tax Filing Form (PND 51) and Annual Corporate Income Tax Filing Form (PND 50).

Who Needs to File It?

Corporate Income Tax (CIT) is a direct tax levied on registered companies in Thailand, which includes legal entities or partnerships operating in Thailand or operating elsewhere but earning certain types of income in Thailand.

Related: General: A Step-by-Step Guide to Registering a Company in Thailand on Your Own

The following types of companies are liable to file the PND 51:

- Any company, juristic partnership, or joint venture incorporated under Thai law

- Foundations or associations carrying on revenue generating business in Thailand (there are some exemptions for charities and foundations under Section 47 (7) (b) of the Revenue Code)

- Companies or juristic partnerships incorporated under foreign laws and carrying on business in Thailand or other places including Thailand, including cases where an employee, an agent or a go-between carries on your business and generates income or profits in Thailand

There are special exemptions on corporate income tax for BOI companies.

BOI companies must prepare the Por 1-2549 Application form for Exercising Corporate Income Tax Exemption Rights and Benefits for the Accounting Year, which must be audited by an external auditor before delivery to the Revenue Department and BOI. However, profit from non-BOI activities is taxable and must be included.

A local accountant can help you with the auditing process.

Learn More: How to Set Up a 100% Foreign-Owned BOI Company in Thailand

How to Prepare PND 51

You can get an English copy of the PND 51 form from the Revenue Department website.

Within the form, you need to list out information from your financial statements, including the company’s projected net profit which is the sum of projected total revenues minus total projected deductible expenses.

Another useful link: Get the Right Company for Accounting Service in Bangkok, Thailand

Corporate Income Tax Rate

Corporate income is taxed at 20% of the company’s net profit.

However, if the company is categorized as a Small and Medium-sized Enterprise (SME) with paid-up capital not exceeding THB5 million and revenues not exceeding THB30 million for the fiscal year, the tax rates are as follows:

- Net profit ≤ THB 300,000 – Taxed at 0%

- Net profit of THB 300,000 – 3,000,000 – Taxed at 15%

- Net profit ≥ THB 3,000,000 – Taxed at 20%

At the end of the form, you need to fill out the total amount of tax you need to pay or return.

Supporting Documents for PND 51

To prepare the PND 51, you need to send all of the following to your accountant:

- Your company’s expected expenses and income for the entire year. If your company is expected to generate no revenue, notify your accountant accordingly

- Actual sales and expenses for the initial six months of the year

- Income and expense projections for the second half of the year (July to December)

- Copy of the PND 50 you submitted to the Thai Revenue Department for the previous accounting period

For cyclical businesses, projections for expected sales later in the year should be adjusted accordingly.

After that, the accountant will fill out the PND 51 and send it to the Revenue Department.

How to File PND 51

There are two ways you can file the PND 51. You can file it on paper at your local Revenue Department. Or you can e-file it through the E-Filing website.

You just need to choose the PND 51 form and file it digitally.

After that, you can save the file to your company for a record. It is suggested to save your company tax documentation for a minimum of five years.

If your company does not yet have a username and password for e-filing, you can use this website to fill out the Por. Or. 01 request for e-filing.

If you use an accountant to open your company and register for VAT, they may have already created an account for you.

Tip: E-filing is much more convenient, and most companies have shifted to e-filing already. In addition, you can also file other types of corporate tax through this website as well, such as the annual tax return (PND 50) and the PP 30 VAT return.

One practical note: filing online through the e-Filing system gives you an 8-day extension beyond the standard August 31 paper deadline, which can be useful if your accountant needs extra time to finalise the figures.

Learn More:

- Taxes You Have to Deal with as a Business Owner in Thailand

- General: How Long Should You Keep Company Documents?

Can I File it Myself?

Although it’s possible to do it yourself, it’s better to hire an accountant to prepare and file the PND 51 form for your company, to prevent any penalty for filing incorrect information.

The accountant can also help you talk with a Revenue Department officer when they have any questions with the form – which is really helpful unless you can speak Thai fluently.

Learn More: The Complete Guide to Learning Thai Online And Available Courses

How to Pay Tax

After you file the PND 51 form, you can pay tax directly to a local Revenue Department or make a bank transfer. QR payment is now also available.

How to Get Tax Return

To get a tax return, there are three options: it can be in cash (if you file it at a local Revenue Department and for small refund), via bank transfer, or get a tax credit for tax filing next month.

Learn More: Increase Your Chances of Getting Tax Refunds

When to File Your Half-Year Income Tax Return

The following deadlines for corporate income tax filing apply to companies incorporated under Thai law:

- PND 50: Within 150 days from the last day of an accounting period or within the month of May

- PND 51: Within 2 months from the last day of the 6-month accounting period or within the month of August (excepting the company’s first accounting period which has a duration of less than twelve months).

Another helpful link: When and How to File Taxes as a Business Owner in Thailand

Late Fines

It is important to complete the Half Year Income Tax Return on time to avoid penalties, and accurately to prevent having to file amended returns.

There are severe penalties for not filing company taxes according to schedule as follows:

- Late filing incurs a minimum fine of THB1,000 and maximum fine of THB2,000

Furthermore, these criminal fines and surcharges are not deductible in the calculation of corporate income tax.

When the semiannual tax return is forecast inaccurately compared to the annual corporate net profit, there are additional fines.

If, at the end of the year, the estimated net profit is found to be less than the actual net profit by 25% or more without justifiable reason (eligible reasons from a legal standpoint are delineated in the Revenue Department Director-General’s Instruction No. Paw 50/2537), the company will be charged 20% of the outstanding tax – a fee which can only be reduced if certain conditions are met.

Another helpful link: Taxation in Thailand: 6 Common Mistakes

Amended PND 51

One tip for filing the PND 51 is to slightly overestimate sales or slightly underestimate total expenses. The Revenue Code permits underestimating profits by no more than 25% of the actual profit results.

Companies that forecast lower annual profits for their half-year tax return and end up with profit 25% or higher than forecast at the end of the year will be required to pay an extra 20% tax on the difference between forecast and actual figures.

If the estimated taxable profit declared in the PND 51 is less than 25% of the actual net profit being declared in the PND 50 at the end of the year, the company can file an amended PND 51 (and increase the estimated net taxable profit in that return in line with the profit shown in the PND 50).

While this will result in a 1.5% monthly surcharge on the estimated net profit difference (between the original and revised PND 51), it will save your company from the 20% surcharge on underpaid half-year tax.

A practical safeguard used by many accountants: if the company pays mid-year tax equal to at least half of the tax it paid in the previous year’s PND 50, the Revenue Department treats this as a reasonable cause, and the 20% surcharge will not apply.

What If I Need to Close the Company?

In the event that you close down your company, you need to file the following forms to notify the Revenue Department to cancel the company inside their system otherwise they will continue to send you reminders for filing corporate income tax:

- Lor. Por 10.3

- Liquidator’s ID card or passport

- Company affidavit with closed status

Learn More: Get the Right Company for Accounting Service in Bangkok, Thailand

Now, on to You

Handling company accounting in Thailand – filing annual tax returns and half-year tax returns – can be complex, especially if you don’t speak Thai. Become aware of the tax returns you are liable to file as a business owner, and don’t fall prey to common accounting mistakes.

Remember that with the help of local accounting firms who know the ins and outs of the Thai accounting system and are experienced in dealing with the Thai Revenue Department, you can stay in compliance with little to no headache even without a large accounting budget.

Disclaimer: This article is written to give you an overview of the PND 51 only. We strongly recommend you to hire an accountant to handle it and prevent any mistakes. In most cases, it should be included in your annual tax filing fee.