This article will take approximately 49 minutes to read. Don't have the time right now? No worries. Email the ad-free version of the article to yourself and read it later!

Travel insurance: It’s that checkbox you tick when you book a flight. Or that free perk on your credit card. Or it’s SafetyWing, World Nomads, or whatever else you saw getting a glowing review on that other website.

But here’s the thing: ticking the wrong box can leave you footing a big bill. And who has time to read up on this for an hour so you know once and for all how to spot good travel insurance? And don’t even get me started on 53 pages of fine print.

That’s why we put together a travel medical insurance comparison tool that takes your details and tells you what the best deal is. Instantly. Go get a free quote for yourself here (no login or email required).

If you do have some time though, keep reading to learn why airlines, credit cards, and bloggers might not be giving you the full story, how to get real coverage without wasting a cent and why it’s a good idea to do so. By the end of it, you’ll be the first person your friends will ask when it comes to travel insurance.

Contents

- Do You Need Travel Insurance?

- Do You Already Have Travel Insurance? If So, Is It Any Good?

- Travel Insurance Vs. Travel Medical Insurance Vs. Travel Accident Insurance

- Should You Get Travel Insurance or 'Real' Health Insurance?

- Do You Need to Buy Insurance in Your Home Country?

- My Personal Travel Medical Insurance Recommendations

- ACS

- Genki

- Dr. Walter

- BDAE

- Getting Sick

- Restrictions on Age, Nationality, Residence and Destination

- Restrictions on Activities

- Trip Cancellation or Delays

- Delayed or Lost Baggage

- Theft, Damage and Robbery

- Death and Repatriation

- Drugs and Alcohol

- Terrorism, Nuclear Fallout and Acts of War

- Pre-Existing Conditions

- Pregnancy and Children

- Arbitration and Disputes

- Personal Liability

Do You Need Travel Insurance?

Travel mishaps are a fact of life. Beyond the odd flight delay, consider the potential cost of getting sick abroad or needing an emergency airlift. Medical evacuation from a remote area, for instance, can easily set you back over $50,000. Skipping insurance could mean gambling tens of thousands to save the price of a nice dinner.

Sometimes, it doesn’t take much. ExpatDen’s founder, Karsten, once took a clumsy tumble on a beginner ski hill. One ski cut into his leg, and he ended up needing staples. Not so bad – except it happened in the U.S. and at a skiing are where there was no Uber, no taxi, and an eight-hour wait for the ski shuttle, with blood pooling under him. A quick ambulance ride and a few stitches later, he was good as new, but the bill was nearly $5,000. Thankfully, the travel insurance plan he bought for that trip (World Nomads – see the full review here) covered skiing injuries, saving him from a nasty financial hit. Karsten is sold on travel insurance, and he thinks you should be too.

But there’s many other ways a trip can go wrong.

Sickness

Ever notice how illness strikes just when you least expect it? Chikungunya, dengue, malaria, traveler’s stomach – the list goes on. Falling ill abroad is more than uncomfortable; it can be frightening, especially when you’re unsure of what’s wrong or where to go.

With travel insurance, you can head straight to a reputable hospital without second-guessing the bill. Top-tier hospitals in some regions can charge six to ten times what a local clinic might, leaving travelers tempted to gamble on cheaper, less reliable options (or to just wait it out). Insurance removes that burden, letting you focus on getting the care you need, fast.

Accidents

Accidents can and do happen. Road accidents involving bikes, cars, buses–we’ve all heard the horror stories because they are true. Outdoor adventure mishaps? Same thing. It has become a badge of honor to compare near-death experiences.

Even the silliest of accidents can happen. My daughter was in Costa Rica spent the day jumping off waterfalls into lakes. But that’s not how she got injured. Nope, she tripped while walking on the road back to her hostel and needed stitches and antibiotics. The medical bill costs four times as much as her day out.

Emergency Medical Overseas and Emergency Medical Transport

Now, this is where it gets really meaty. Yes, ICUs, Strokes and Comas are expensive. But those seem kind of rare and require you to be in a state in which you are damaged to the point where your life afterwards will not be the same.

But you don’t have to be so badly injured to rack up an inordinate amount of debt:

A good friend of ExpatDen’s founder tripped and fell over the side of the walkway because railings are apparently a thing they don’t always do on small islands in Thailand. He broke his hip. Not the worst thing that can happen to a 30 year old. But how do you get treated?

In his case, with an excruciating speed boat ride to the next hospital. There they first checked if he had travel or health insurance before even letting him in (maybe the Hippocratic Oath is phrased differently in Thai). But that small island hospital had in no way the facilities to operate on him. His insurance ended up chartering an entire airplane (as in, the Boeing 737 kind) to fly him to Bangkok where he was operated. Despite being in a world class hospital, treatment didn’t go well and he contacted his insurance who flew him out again – this time back home to Sweden, where he made a full recovery.

Medical evacuation easily costs a few ten thousand dollars, even if you’re injured in a ‘convenient’ location. But if you’re in a hard to access spot, it can reach six figures. Hard to access might even be just a short half-day hike or bike ride: Many kind of injuries (think: spine) mean you can’t just be carried back and they’ll have to call a helicopter.

I saw this first hand in a hospital in India where a British guy was fixated on a bed with a metal framework holding him still, waiting for medical evacuation back home: He and his girlfriend had a bike accident and the visor of her helmet hit his spine, injuring it. They didn’t have any insurance.

Skin Infections

Going tropical? So might your skin. A change of climate can quickly result in eczema, athlete’s foot, reactions to insect bites, and more. Okay, so why not just get over-the-counter-(at-least-in-Thailand) cream to handle that?

I’ll tell you why: I had a mosquito bite in Sri Lanka that resulted in blood poisoning after getting infected from the humid environment. Not fun. And certainly not a situation where I would want to delay seeing a doctor because I’m worried about what it might.

Travel Disruptions and Cancellations

From a family member becoming sick and you needing to rush home unexpectedly to getting sick yourself and not even leaving for your trip in the first place, there are many reasons why travel plans get disrupted. Especially if you’re traveling with family, the odds of someone in your party getting sick increases exponentially.

More importantly, airlines might reimburse you for the cost of a cancelled flight, but most certainly not for the cost of the cruise you’ll miss because of that. Remember last hurricane season? If no flights leave your airport and you miss out on a Disney vacation, that’s really an experience I wish on no family.

Theft, Loss, and Damage

You don’t just have to worry about medical issues.

You could leave your passport in a taxi (my sister), have a phone pinched from your pocket on an MRT train in Singapore (my daughter), have a camera taken from a suitcase while on a bus in Indonesia (me), or be mugged on a London street (also me).

There is no accounting for the number of reasons why you might experience theft, loss, or damage to your personal items while traveling. These might not be life or death experiences, but they are very real annoyances that can be time-consuming and expensive.

Travel insurance doesn’t prevent any of the above from happening, but it does protect the financial investment you made in the cost of travel and the health and personal items you travel with. The commonly held view is that if you can’t afford travel insurance, you can’t afford to travel. And you most certainly can’t afford anything to go wrong on your trip.

Convinced? Find out what the best travel medical insurance is for your age, home country and destination: Get an instant quote from insurance companies we handpicked for you.

Do You Already Have Travel Insurance? If So, Is It Any Good?

This is something you really want to consider because no one likes paying for something only to discover they already have it. Let’s take a look at where you may already have some travel insurance coverage.

Airline

Airline “Add-On” Insurance

It’s become trendy (read: profitable) for airlines to offer “travel insurance” at checkout. It’s convenient – a single click, a small fee, and you feel like you’ve checked “buy travel insurance” off your list.

But did you read the exclusions? How much you’ll need to pay yourself if something goes wrong? Does it actually cover medical costs or just accidents in which you lose a limb? Who is actually selling you that insurance (hint: it’s not the airline)? If you didn’t read that, so did no one else. Airlines know this and so they don’t have to offer a particularly good or even halfway competitive deal.

In fact, they just have to offer a cheap deal (to make you buy) and negotiate a high commission for themselves (which the provider pays, because they certainly are unlikely to ever have to pay out an expensive claim).

Travel insurance on the airline website is about as useful and as overpriced as the extended warranty at Walmart: You always want to say no to that.

Credit Cards (for Everyone)

Some cards offer benefits including complimentary personal accident coverage, travel insurance, and medical assistance. Depending on where you are based and what card you are able to take out, you may have some similar benefits on offer.

It’s worth noting, however, that if you find your credit card does have some travel insurance, it’s likely only accessible if you’ve booked and paid for all or part of your travel using that card. Especially if you want to rely on credit card coverage alone, make sure you read and understand the fine print around the benefits carefully.

Because here is a thing most people miss: Coverage from credit cards usually only applies to non-medical costs. When they say ‘travel accident insurance,’ they’re talking about serious scenarios—think loss of life or limb. If you end up in an accident but still have all limbs attached, coverage won’t likely apply

Where credit card travel protections really shine though are trip delay and cancellation benefits as well as medical evacuation – this saves you having to buy those as extra add-ons when you get proper medical travel insurance. It’s a major reason I only use cards with good travel insurance when booking flights.

Even if you already have travel insurance, you might want to consider getting a travel-oriented credit card anyway. “Normal” credit cards add something called foreign transaction fees on any money you spend abroad, which can cost you 3% on top of every transaction.

Credit Cards (For Americans)

While the above credit card section applies to everyone. This part is U.S. specific: Americans have access to an entirely different level of credit cards when it comes to travel bonuses, so the case for getting one is even stronger than elsewhere.

Take the Bank of America Premium Rewards card: It costs $95 annual fees, but you get $600 for signing up if you spend $4,000 in the first 3 months. If you haven’t paid for your trip yet, that’s not just an easy way to get non-medical travel insurance, but an extra $600 spending money on top. You’ll find this card not mentioned very often on credit card blogs because Bank of America doesn’t pay commissions for websites sending them new customers, but it’s a complete no-brainer if you can get it.

Another credit card in the same price range that also includes rental car insurance is the Chase Sapphire Preferred (CSP).

More expensive credit cards usually come with travel insurance. The difference between cheaper cards and these cards tends to be the limits on what is covered and how easy it is to use the benefit. Chase Sapphire Reserve (CSR) costs $795 a year and pays out if your flight gets delayed by 6 hours or more, whereas the cheaper CSP requires a delay of at least 12 hours.

When it comes to a credit card that has medical treatment coverage, such as, The Chase Sapphire Reserve. These cards generally come with limited coverage. For example, The Chase Sapphire Reserve can cover you only up to a grand total of $2,500. Good luck with that if you ever get admitted to Bumrungrad Hospital. It is a nice perk to have for smaller injuries or illnesses though.

Bank Accounts

In some countries you get travel insurance with your bank account – especially outside the U.S. this is something I’ve come across quite frequently. Whether that’s a good deal or not, depends a little on which country you are in. Some nationalities never use their insurance (e.g. polish guest workers traveling to Germany) and thus banks and other institutions hand those out quite freely. Regardless where you live though, make sure you are covered for medical costs and make sure the coverage actually lives up to what you need.

Car Insurance or Other Insurance Products

Likewise, if you have car or contents insurance in your country of residence, you may find that there is some limited coverage for having your bag stolen when on holiday or having an accident while driving in the country you’re vacationing in.

This level of coverage is likely to be limited to specific items or occurrences outside of the country where you have taken the coverage out, so it may not provide full coverage and shouldn’t be considered a substitute for travel insurance.

Travel Insurance Vs. Travel Medical Insurance Vs. Travel Accident Insurance

When looking at travel insurance, you will sometimes see policies described as travel insurance or travel medical insurance. Sometimes it’s even described as accident insurance.

What’s the difference?

- General travel insurance might only cover non-medical costs – delayed flights, cancelled tours and lost luggage. This is something you often find bundled with credit cards or other products.

- Travel medical insurance on the other hand covers you if you need to see a doctor or get admitted to hospital. This is actually the most valuable part of any insurance package and you’ll never see it bundled with other products as a small benefit. When we compare travel insurance plans, this is the primary thing we pay attention to. Try it out yourself.

- Accident insurance can mean everything and nothing: In the case of credit cards, it means accidents where you lose a limb or die. I would ascribe no value to this unless you are in the incredibly unfortunate position of having lost a loved one and have to figure out what your rights are.

What can be very confusing is that people tend to frequently use ‘travel insurance’ as a catch-all to refer to any or all of the above. When somebody says ‘They should have bought travel insurance’ you would need to know the context to know whether they meant the flight-is-late insurance or the hospital-stay-is-covered-insurance.

Should You Get Travel Insurance or ‘Real’ Health Insurance?

Some long-term travelers or digital nomads might be trying to figure out whether they can get away with travel medical insurance (which is significantly cheaper) or a traditional health insurance plan.

Let’s say you decided to spend a gap year in Thailand. Should you pick a normal health insurance or a travel medical insurance?

The main differentiation between the two is that travel insurance pays for unexpected expenses and health insurance pays for all expenses. Having pregnancy complications is an unexpected medical expense and *might* be covered by travel medical insurance (depending on the policy). However, going to a routine pregnancy checkup is expected and would not ever be covered by travel medical insurance – but a normal health insurance plan can cover it if it includes maternity benefits.

Another point is renewals: Health insurance is on the hook if you develop a chronic illness while covered and any decent plan will not be able to kick you out. Travel medical insurance might limit covering treatments for a certain duration after the initial incident during which you are covered for followup care. After that you are on your own.

If you are in the situation where you find yourself in a gap year or temporary stay abroad, I’d use the following criteria: Are you going to stay in the country even after a serious accident or illness? In that case, get proper health insurance. Would you go home to seek future treatment there once you’re cleared for travel? In that case, travel medical insurance will work and can save you a lot of money

If you want to go a little deeper into the considerations, pros and cons and how to go about making a good choice when staying abroad for a longer period of time, check out our article on health insurance for digital nomads or use the quote tool here to find out which company offers the best policy for long term travel and extended stays.

Do You Need to Buy Insurance in Your Home Country?

Nope. Often it’s even advisable to specifically not do that. Let’s have a look.

Local Providers

An online search for travel insurance will reveal a plethora of options depending on where you’re doing your search. For me, sitting in Singapore, even when I search for international travel insurance, I see plenty of local health insurance companies. These are travel insurance plans offered by Singapore companies like FWD Insurance and linked to me being resident in, and therefore traveling out of, Singapore for my trips.

But you don’t need to buy travel medical insurance from an insurance company in your home country. In fact, you can buy it from nearly any company in the world – often opening up much better conditions or lower prices. Think about it – what are the odds that the one company that offers the best plan for your situation is actually located in the same country as you?

International Providers

Some companies and plans are only available to residents or citizens of specific countries. The FWD plans mentioned above are only available if you’re a resident of Singapore. Pro Trip by Dr. Walter (amazing plan by the way) is only available to Germany citizens.

However, many other plans are available to anyone, anywhere – sometimes with some embargo exceptions, so if you’re living in Iran, your options in this category are probably very limited. In my experience, the best value for money tend to be European insurance companies – ACS, Genki (which is a reseller of Dr. Walter) and BDAE stand out as particularly amazing.

One thing to keep in mind though with international companies is that they’ll follow different insurance regulations than in your home country or require you to dispute claims in their home country. Here’s a Reddit post looking into a travel medical insurance company called Ekta. Spoiler: Ekta is based in Kiev, Ukraine and if you want to dispute a claim with them, you have to do it in court. In Kiev. In an active war zone. No thank you.

However, it can also be the other way round. If you buy from a company that’s located in country that’s very consumer friendly – France and Germany come to mind – you get way better protections than what you would most likely find in your home country.

My Personal Travel Medical Insurance Recommendations

Especially in the digital nomad market, there have been a few brands in the last few years that really created a following. Let me rephrase. A few companies realized that if they not only pay commissions to insurance agents, but everyone who says nice things about them online, they’ll get praised to high heaven. That doesn’t necessarily mean these companies are bad, but it certainly means you should read any praise you find online with a grain of salt.

That includes ExpatDen. We also earn commissions from insurance companies, whether or not we give them glowing reviews. Since insurance pricing is standardized, it doesn’t cost you any extra. We do our best to stay unbiased, keeping our focus on giving you the real story. But it’s important to us that you’re aware of this.

World Nomads

World Nomads has an extremely comprehensive global travel insurance policy but the coverage and benefits will differ slightly depending on your nationality and country of residence, in particular, if you’re from or live in the USA, Canada, Australia, NZ, Europe, or Brazil.

Karsten – founder of ExpatDen – used them for a trip to the U.S. As he was I was lying on a bed at the first aid station at a skiing resort near Seattle, he tried to figure out what options he had and called them up: “Someone immediately answered the phone and confirmed that all of my expenses would be covered – regardless which hospital I went to and regardless if I was driven there or took an ambulance. It was a massive relief”.

World Nomads is especially good if you’re looking for flexible travel insurance as you’re able to purchase it online at any time and can extend your policy should you decide to keep traveling beyond your original policy end date.

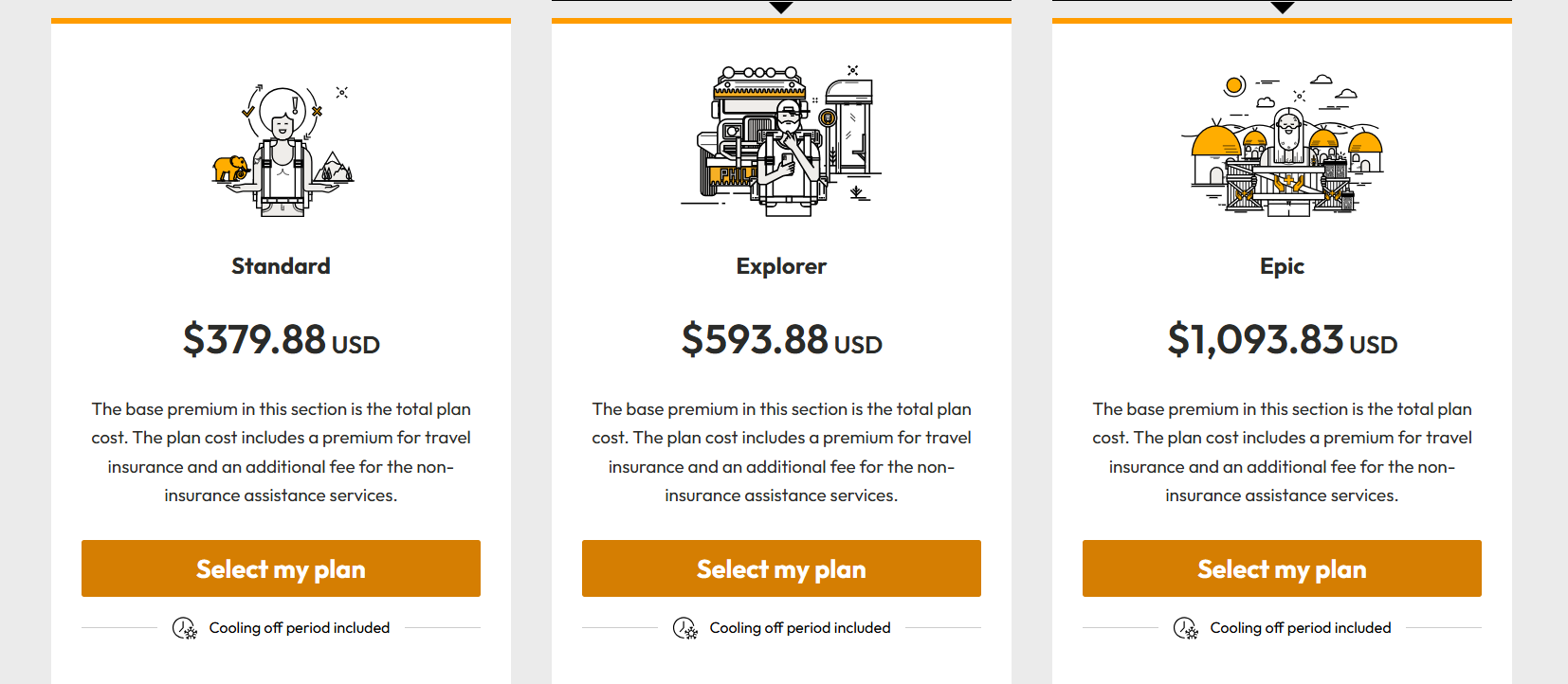

World Nomads offers the option of either a Standard or Explorer policy, the difference being in the level of benefits. Karsten went with the Explorer policy and was thus covered for skiing accidents (which wouldn’t have been the case for the Standard plan).

I ran a quote through its system for three months, traveling around Asia as a 32-year-old, and came up with the following:

And here’s a quick overview of the coverage for the standard plan:

- Accident and sickness: US$125,000

- Medical evacuation: US$400,000

- Baggage and personal effects: US$1,000

- Trip interruption: US$2,500

Holy moly. That’s some serious coverage. $400,000 for medical transport? At that point you don’t have to worry – even if the insurance has to charter an airplane to get you to a hospital (happened to a friend of mine on Koh Samui – he got a chartered flight to Bangkok after breaking his hip). The Explorer plan pays for missed connections, reimburses you money that was stolen from you and even has your back if you lose the keys to your rental car.

Verdict

World Nomad’s kind of coverage doesn’t come cheap though. The Standard Plan at US$379.88 and the Explorer Plan at US$593.88.45 are significantly more expensive than most other options. Coverage comes at a price, but if you want to get some of the best coverage money can buy, World Nomads seems to be a safe bet. Nowadays I probably would look for something cheaper for myself, but if I had a friend who is nervous about traveling, I would send them to the World Nomads.

SafetyWing

SafetyWing gears itself as travel insurance for nomads, but they also offer one-off travel plans – which in some cases can be way better deals than anyone else. You can roughly divide SafetyWing’s travel medical insurance offerings into the following categories:

- One off (you prepay for the entire, specific duration of your trip – useful for shorter trips)

- Subscription (automatically renews every 28 days – useful for perpetual travelers)

If you’re between the ages of 18 and 39, prices starts at US$62.72 every four weeks.

In my eyes, the SafetyWing subscription falls a little in between a traditional health insurance and a travel medical insurance. Unlike travel medical insurance, it can be perpetually renewed whereas most travel medical insurance companies only offer a one year or two year maximum (notable exception being BDAE, which offers up to 3 years). However, renewal is conditional on the approval of SafetyWing. You might see where this is going: If you become a long-term liability for them, they have every incentive not to renew your coverage.

Another nice feature is that visits to your home country are covered for up to 30 days (15 if you’re from the U.S.) after you’ve had 90 days of continuous coverage. While home country coverage isn’t super rare, not every insurance company offers this and it’s nice to know you’re covered when flying home for the holidays (especially if it’s the U.S.!).

The most powerful feature in my eyes is that two children under the age of 10 can be added for free as part of a family package. This is a game changer if you’re traveling longer with children in tow as it can seriously lower the overall cost of coverage. ExpatDen’s founder Karsten recently purchased this policy for his family of 4 because there was no other plan remotely in that league once he took into account that both of his kids were covered for free.

SafetyWing’s coverage limits are sufficient, but are stretching it a bit for high health cost destinations like Switzerland, Canada and the U.S.:

- US$250,000 as an overall maximum coverage limit

- US$100,000 lifetime maximum for emergency medical evacuation

- US$5,000 for trip interruption

- US$500 per item of lost baggage up to US$3,000 per certificate period

On the plus side, these coverage limits though mean that it’s a lot less expensive than World Nomads.

Given it’s a U.S. company, it’s not surprising that SafetyWing policies are available to anyone unless your home country is Iran, North Korea, or Cuba – or if you hold Cuban citizenship.

Verdict

All in all I’d say SafetyWing provides decent coverage that you don’t have think about much if you’re a solo traveler. If you’re a family with young kids, there is a good chance it’s the best policy in the market for you.

Famous actors out of the way, let’s get to the insurance companies I frequently find myself recommending to my friends and relatives. Each has their own pros and cons, but usually at least one of them is a great fit, regardless of who you are and where you are going.

ACS

ACS is a French insurance company that has made a name for themselves with travel medical insurance in Europe and very competitive expat insurance offers in South East Asia. They’re not widely known outside these regions – which is a real shame: Their Globe Traveller plan is the best I’ve seen for anyone under 66 years old heading to the United States.

The Globe Traveler policy is available to all nationalities and offers a customizable approach, with three levels of maximum medical coverage to choose from: €150,000, €300,000 and €500,000. Prices range from €41.60 to €114.40. If you’re heading to the U.S., I recommend going with the middle or higher coverage tier.

A nice touch here is that ACS offers direct payment for hospital stays of more than 24 hours. Pretty handy when faced with astronomic hospital bills. I’m a credit card points chaser, but once the bills hit 5 figures, I get uneasy paying in advance and waiting for reimbursement. Direct payment means I don’t have to worry about that. Speaking of not having to worry: There are deductibles on health care expenses, making you much less likely to skip a doctor’s visit if you’re on the fence.

At their price point it also really stands out that in addition to covering 100% of actual costs for emergency medical transport or repatriation, the Globe Traveller plan will also reimburse you for up to €2,000 for baggage theft, loss, or destruction. If you’re bag arrives late (meaning more than 24 hours), they’ll reimburse you €150 to cover basic necessities. The 24 hours waiting period is a bit too long for my taste, but given that there are credit cards that pay after 12 or even as little as 6 hours, there’s an easy way to cover that risk.

If you ask ACS to talk about themselves, they’ll tell you that they work with well-known and recognized partners such as Allianz and AXA and has been serving international travelers for more than 40 years. Sounds nice. I’m not sure how to put those statements into context though. It does seem to back up the reputation they have for the people I talked with though.

One downside: Globe Traveller doesn’t cover flight cancellations within the standard package, only delays, so if you want this (and you’re not getting it through your credit card) you have to add it as an option. Likewise with any adventure sports or equipment coverage.

Globe Traveller is included in our travel medical insurance comparison tool, so you can see how it stacks up against the other plans.

Verdict

ACS’ plans are very good for most people under retirement age, but where they really stand out is if you travel to the United States. The plan also comes with good medical coverage at affordable price.

Genki

In order to understand Genki, you need to know two things about German insurance companies:

- They offer some of the best insurance plans in the world

- They couldn’t sell water in a desert – marketing just isn’t their thing.

And who can blame them? The common joke is that it’s easier to sell insurance to a German than coke to an investment banker (not the soda kind). So who needs marketing? In Germany? No one. In the English-speaking world? Anyone who wants to compete with World Nomads and SafetyWing.

Enter: Genki. Scouting the (mostly) German insurance market for the best plans it can find, Genki offers the same product under their own brand, adds some proper customer service and sells them to an international audience. How do they make money? Commissions. Same as every insurance broker out there. And what do customers get? A point of contact that understands them and an insurance deal that’s hard to beat.

Let’s have a look at their Genki Traveler Plan for example:

- Age: 0 to 69

- Medical Coverage: EUR1,000,000

- Price: from €1.75 (approx. $1.90) / day

- Duration: Covers trips for up to 1 years

- Can be cancelled anytime

- Can be booked after departure

Verdict

Genki Traveler is a really solid plan. ACS sometimes offers a better deal, so it still makes sense to compare, but Genki is a great go-to option if you just want something that always delivers a very good deal without having to compare offers every time you go travel.

Find out more: Genki Traveler Review: Pros, Cons, What’s Covered, and What’s Not

Dr. Walter

Dr. Walter started out as a German insurance broker that eventually packaged and sold their own insurance products. Their Pro Trip World plan is the one I pull out when I want to blow people’s mind how cheap comprehensive coverage can be. Here are the facts as provided by SafeAndNotSorry page on Pro Trip World:

- Age: 0 to 69

- Medical Coverage: Unlimited

- Price: from €3.9 (approx. $4.5) / day

- Duration: Covers trips for up to 1 years

- Can be cancelled anytime

- Can be booked after departure

- Can be extended for 90 days if you fall sick towards the end of your trip

Verdict

Price-wise and price-for-value, Dr. Walter Pro Trip World is unbeatable – the only exception being families with young kids where SafetyWing offers a better deal. For several destinations, Dr. Walter Pro Trip World and Genki Explorer cost the same (because it’s the “same” plan), but that doesn’t always hold true. It does have limitations in that it might not be suitable for perpetual travelers or people going to the United States, but everyone else is getting a great deal.

BDAE

Alright, between other companies offering insurance up to age 74, €300,000 coverage and prices of barely less than 2 dollars a day – why would you even need another recommendation? Easy answer: Duration. While there are companies that offer unlimited duration (e.g. SafetyWing), they can kick you out at every yearly renewal. That would be a real bummer if you just relocated somewhere with your entire family.

And this is where BDAE comes in. Another German insurance company (of course). Their Basic plan allows you to get travel medical insurance for 3 years. That can cover an entire job posting abroad, an entire undergraduate degree or enough time to become a digital nomad until there’s a new president back home.

Verdict

It’s not the cheapest plan, but come with high coverage (typical for Germany, again) and the peace of mind knowing that you got your insurance sorted out for the next 3 years is hard to beat for long-term travelers. With a maximum age of 74 it’s definitely not for retirees, but everyone else who is staying abroad long-term could consider this.

How Much Does Travel Insurance Cost?

Non-Medical Travel Insurance

If it’s just for non-medical costs, you can get pretty good coverage with a premium credit card. Expect to pay about $95 in annual fees for those cards – or the equivalent thereof in the currency of your local country. Given the sign-up bonuses of many credit cards, these pay for themselves in the first year, so essentially you can get this for free. Americans have the best options here – see the credit card section for more details.

Travel Medical Insurance

Things get more expensive if you’re looking to be covered for medical care. Prices start around $1.12 / day if you’re a younger adult and frequently will cost more than $10 a day if you’re well beyond retirement age.

Travel Insurance Fine Print Explained

While buying travel insurance can be as quick as the click of a few buttons, understanding what you’re buying could take a little longer. Two policies might look similar at the outset, but they could differ once you get into the nitty-gritty of their benefits. This is really what to watch out for when you dive into the 30+ pages of fine print to compare two insurance plans. I don’t think it’s necessary to understand all of these details – but if you see an offer that looks too good to be true, this is where you’ll usually find out why. Let’s take a closer look.

(alternatively, skip this and go with any of the recommended insurance companies and plans I listed above – these were already vetted on those criteria)

Getting Sick

Travel insurance will cover you for unexpected illnesses or injuries that need to be treated in the short term. This is pretty standard. What varies is how long they’ll treat you after the accident. Have you ever wondered what happens if you have an accident on the last day of your insurance coverage? Most insurance companies have phrasing that says how many days they’ll extend your policy if you are in treatment. But the exact number of days can vary.

Restrictions on Age, Nationality, Residence and Destination

As it suggests, restrictions may limit who a policy is available to. The most common restrictions are country of residence, nationality, age and destination. If you live in Iran, North Korea, or Cuba, you won’t be able to buy a SafetyWing policy while, ACS Globe Traveler is restricted to those under the age of 66.

The most common restriction in these categories are maximum age, embargoed nationalities and countries, as well as particularly expensive destinations. The U.S. is first among those, often (but not always) mentioned with Canada in the same breath. Recently I’ve also seen the UK and Switzerland added and from what I hear from friends in the insurance industry, some Asian nations like South Korea and Japan could also make the list in the future.

Usually you don’t have to worry about these restrictions, as insurance won’t be selling a plan to someone that doesn’t meet those requirements. If you lie, they might accept you, but once you file the first serious claim they’ll go over everything with a fine toothed comb and most likely annul your coverage.

Restrictions on Activities

This one makes sense to look up yourself if you’re going to do anything more exciting than a bike ride or a hike. From climbing to skiing there are a lot of adventure sport exclusions – and these vary between every single insurance company.

There are only two ways to figure out if an adventurous activity you have planned is covered: Read the fine print yourself, or ask someone who did. This contact form goes to that someone.

Trip Cancellation or Delays

This is the one that always trips people up when their flight gets cancelled or they miss their connection – only to find out that their insurance doesn’t pay. Here are the most common reasons (in the fine print) that’ll result in claim rejections:

- Someone else is responsible to reimburse you. They don’t always tell you that, but if there is another party that should be reimbursing you (e.g. the airline) this is often directly or indirectly excluded. The way to indirectly exclude it is to only offer the benefit for scenarios where the airline doesn’t have to pay. This is good news: It means you’ll still get reimbursed, you just asked the wrong company.

- There is a minimum duration requirement. “Delayed” is a vague term. Fine print specifies if it means 3 hours, 6 hours, 12 hours or 24 hours. If you still arrive earlier than that: No delay, no reimbursement. Atlas Travel Insurance covers you after you’ve been delayed for 12 hours and then only for up to two days. Chase Sapphire Reserve on the other hand pays out after only 6 hours of delay.

- Consequential damage. If your flight gets cancelled and you need to buy a new ticket to get to the destination, that’s incidental damage. If you miss the departure of your cruise because of that, that’s consequential damage. Unless specifically mentioned, travel insurance does not cover consequential damage. This is probably the single most important point if you’re getting insurance because you lose a lot of money if something goes wrong on your journey.

This right here is what sets good insurance apart from bad ones: How restrictive are sections like this phrased? Your friend who doesn’t like an insurance because the company rejected his claim? Most likely it was something like this in the fine print.

So what does insurance in this category usually cover? In a nutshell: Hotel, food, clothing and transportation if you miss a connection have to stay overnight as well as the cost of the previous ticket if the airline doesn’t refund it for some reason.

Delayed or Lost Baggage

Delayed or lost baggage is another problem that causes much anguish. I’ve had bags turn up a week late and soaking wet thanks to someone leaving them on the runway in a rain storm. It’s not ideal, so you definitely want your policy to cover you for these mishaps. Check that you’re covered for not just the items you could potentially lose, but also for replacement items that you have to purchase in the short-term. After all, no one wants to see you wandering around in the same clothes for days on end.

Personally I rarely care about this item as I’ve never seen an airline reject a claim involving damages for things I’m willing to put in checked luggage. Even though they might fit it tooth and nail, eventually they always pay. It’s different if you have to check in fragile or electronic goods as those are usually not covered by airline liability.

Theft, Damage and Robbery

You don’t only have to worry about bags getting lost or delayed, you also have to protect all that gear you carry around: your camera, laptop, any sports kits, etc. With your life on your back, you can’t afford for it to all go missing and not be able to replace it. The key thing here is that you’re going to need to prove that all your items were actually lost, stolen, or damaged (a local police report might help), and submit receipts showing the date and cost of all your purchases. It’s always worth getting that kind of paperwork together before you leave.

This is another item where insurance fine print will make it very difficult to claim: Several companies require you to observe the item actually being taken. If you’re distracted and something is suddenly gone or you forget something in a taxi: Quite a few insurers won’t pay. If you carry around very expensive gear, pay attention to the fine print in this section. I’m not into photography and pay everything by credit card, so other than a phone that’s a few years old, I don’t carry much of value on me and don’t particularly care about this.

Death and Repatriation

It’s all getting a bit sombre suddenly, but this is another big one that you need to think about. You don’t want to lumber your family with hidden costs should the unthinkable happen. Again, the more remote and adventurous you plan to be, the more you should consider for your level of coverage.

Drugs and Alcohol

If you fall off your moped because you were on drugs or drunk, don’t expect the ensuing medical costs to be paid. Generally, anything that can be considered a result of your own doing: drugs, alcohol, self-harm, suicide, will not be covered by any insurance policy.

This is tends to be pretty common across the board. Some local companies in South East Asia go a lot further though and will refuse to cover you if there is any alcohol in your blood at the time of the incident and will go as far as hiring a private detective to find out if the claim amount is high enough to warrant it.

Terrorism, Nuclear Fallout and Acts of War

These are pretty commonly excluded for medical costs – I don’t recall any travel insurance covering it.

Pre-Existing Conditions

Travel insurance policies are not health insurance policies and they don’t extend to most pre-existing medical conditions. You’ll need to check the wording of your policy to see if you’re covered or not, as it may depend on the timing of when you were diagnosed. Some policies have what is called a “look back” period, the time prior to purchasing your policy. If a condition was diagnosed, you’re not covered for losses due to treatment for symptoms.

In general though, travel insurance only pays for sudden and unexpected expenses. A chronic disease, a prior diagnosis or an issue that materializes slowly over time usually falls under this.

Pregnancy and Children

If you’re pregnant at the time of booking your trip, don’t be fooled by mentions of ‘maternity/pregnancy’ coverage on websites and marketing brochures. These refer to unexpected complications and often cover you only up to a certain gestation period. Routine and preventive care is never covered by travel insurance. You’re better off getting full health insurance in this case. Most of the insurers mentioned in my recommended insurance companies section have full health insurance plans that do cover this kind of routine car.

If you already have children ages ten and under: SafetyWing allows you to add up to two children (one per adult) for free on your own family insurance plan which could be another alternative.

Arbitration and Disputes

This is the money section of the fine print. Here they’ll talk about what happens if you disagree with what the insurance decides. Sometimes there is an arbitration clause, an ombudsman or other requirement on how legal disputes have to be handled. If you’re in the U.S., small claims court is always an option and can’t be removed in fine print.

How bad this clause can be is something you can see when you look at the fine print of Ukrainian insurance company Ekta: They require you to travel to Kiev, Ukraine to argue your case in a local court. I wonder which travel insurance would cover you for that trip.

Personal Liability

Should you find yourself in trouble for injuring someone else or damaging someone else’s property, then personal liability coverage can be useful to help cover your legal defense or compensation costs. Very often there is a clause that you are not to admit fault (lawyers would say, don’t apologize because that can be seen as admission of fault, even if it’s just a reflex). World Nomad’s has a huge level of coverage – up to US$1,000,000 -within its basic standard plan, but other providers like ACS offer personal liability as an add-on.

Speaking of which.

Add-Ons

Under some policies, you can take out additional benefits to bump up your offering. Some of them are listed below.

Dental

Emergency coverage for dental can often be purchased as an add-on. World Nomads, for instance, will cover you for US$300 and US$500 on its Standard and Explorer plans respectively.

Adventure Sports

Adventure sports is frequently highlighted as an exclusion, but under most policies – like ACS Globe Traveler – you can pay to add coverage for risky sports and losses or damage your equipment.

Cancel for any Reason

This add-on lets you cancel for any reason and helps you work around some of the exclusions a policy might have. There are very few places in the world where this is actually offered and it usually costs an absolute fortune.

How to Make a Claim

So you’ve got your policy, you’re on your trip, and now you need to make a claim. Whatever the reason, be it in an emergency situation or claiming for a delay, there are a few key pointers to remember.

Emergency

In an emergency you might not be in a position to follow specific instructions. But if you can, the following can be helpful. It’ll also help you prepare for this kind of situation.

Have Insurance Details Ready

Have your policy number ready along with a contact number and your location. Best save this on your phone. You probably want to confirm you’re covered before agreeing to an expensive procedure (assuming you it’s not a live or death scenario)

Get the Necessary Paperwork

Obtain any paperwork that you need for the claim. For example, a police report showing proof of a theft or airline tickets if bags have been lost.

Don’t pay for anything without an invoice or receipt and keep them (best take pictures with your phone in case you lose the originals) – this doesn’t apply if you’re in some dodgy hospital that won’t treat you without upfront payment. Pay by credit card in that case.

Don’t Admit Fault

Don’t admit to wrong-doing or fault. This is for the insurance (or the legal system) to sort out and any statements you make can only be to your disadvantage. This is a common clause in insurance contracts and I’m not entirely sure if it is for your benefit or for the benefit of the insurance, but I say better safe than sorry.

After The Fact

You paid out of pocket and are now looking to get reimbursed. Keep this in mind:

File immediately

Many insurance companies require you to file within 30 or 60 days. You might not have all documents or you are still waiting for a decision from the airline. If you wait, you lose all right to a claim. So what to do? File a claim stating an estimated amount and state documentation will be added later. This opens the claim in time and you then can wait for all the other documents to arrive before you file.

Read the Terms and Conditions

Reread the fine print of your policy before you file a claim. Often your claim needs to fall under a category that’s mentioned in the insurance. If you figure out in advance which one that is, you’re less likely to get denied.

Take Your Time

Be aware that how you word your claim can influence the outcome. If you make an incorrect or inexact statement to your disadvantage and get denied, it can be hard to get that reversed. Especially when it comes to describing an incident (and making sure you really included all expenses) you want to make sure you got everything right.

Best Time to Buy Travel Insurance

Ideally, you should buy travel insurance the same day you will book your flights or travel. Some policies are time sensitive and will require the policy to be in place from the outset. Moreover, if you’re considering buying the add-on “cancel for any reason,” you should get this at the same time because you never know when you might need it.

What is the Best Travel Medical Insurance for You?

Enough with the waffling, insights and deep dives on fine print. If you’re anything like me, you probably skipped right away down here to just figure out what the best insurance is and click on it. And I won’t disappoint. Enter your details below and you’ll have your answer.