This article will take approximately 26 minutes to read. Don't have the time right now? No worries. Email the ad-free version of the article to yourself and read it later!

I honestly can’t remember the exact year we opened our Wise Multi-Currency Account. Maybe it was around 2018? Back then, it was still called a Borderless Account and Wise was known as TransferWise.

What I do remember clearly is how much it changed the way we ran our business. Suddenly, paying our international team became so much easier and cheaper. We could just upload a batch file and pay everyone at once in their own currencies. No more juggling different platforms or dealing with ridiculous bank fees. For a full comparison of how Wise stacks up against alternatives, see our guide to sending money abroad.

Fast forward to today, and we’re still using our Wise Multi-Currency Account every month. It’s become one of those tools we rely on without even thinking about it. So in this article, I’ll walk you through everything based on our real experience: what we like about it, what could be better, and whether it’s a good fit for you.

In short, it’s a great option for expats, remote teams, or anyone dealing with cross-border finances. It’s super easy to set up. Just sign up for a Wise account and upgrade to a Multi-Currency Account.

Here’s what we’ve found.

Contents

- Key Takeaways

- How the Wise Multi-Currency Account Works

- Benefits of Using the Wise Multi-Currency Account

- Paying Our International Team

- How the Multi Currency Account works

- Fees

- Transfer Speeds

- Safety and Security

- Ease of Use

- How to Open a Multi Currency Account

- Wise Card

- What I Don’t Like about Wise

- Should You Open a Wise Multi-Currency Account?

- Additional Tips to Get the Most Out of Your Wise Multi-Currency Account

- Alternative Services

- FAQs about Wise Multi-Currency Account

- Is Wise a real bank?

- Can I open a Wise Multi-Currency Account if I just moved abroad?

- How long do Wise transfers take?

- What currencies can I hold in my Wise account?

- Can I use Wise to receive payments from clients or platforms like PayPal or Amazon?

- Is it free to open the Multi-Currency Account?

- Is the Wise Card available in my country?

- Can I withdraw cash from ATMs with Wise?

- Can I use Wise for business purposes?

Key Takeaways

- Wise Multi-Currency Account lets you hold over 40 currencies and convert at the mid-market rate with transparent, low fees rather than inflated bank exchange rates.

- Local account details (US, UK, EU, Australia, and more) let you receive international payments as if you had a bank account in those countries.

- The Wise debit card works in 150+ countries and converts at the mid-market rate when you spend abroad, making it practical for travel.

- Batch payments let you pay multiple team members in their local currencies with a single file upload, saving time for remote teams.

- Wise is regulated by the FCA in the UK, FinCEN in the US, and equivalent bodies globally, with customer funds held in ring-fenced accounts.

- Transfers typically arrive the same day to within 2 business days, depending on the currency and destination country.

- Account holds during identity verification are the most common friction point reported by users; having your documents ready upfront avoids most delays.

How the Wise Multi-Currency Account Works

You can think of Wise as a multi-currency bank account where you can hold and manage over 40 currencies at once, including major ones like USD, GBP, EUR, AUD, and more.

Once you have those currencies in your account, you can:

- convert them to your local currency and transfer to your bank account

- pay others directly in their local currencies

- Use a Wise debit card to pay for things in your daily life.

It’s also a very handy account if you need to do international transfers regularly. You can easily send money to over 160 countries with just a few clicks, often much cheaper and faster than using a traditional bank.

And if you plan to live abroad, in my opinion, a Wise Multi-Currency Account is one of the most useful things you can have. It makes it so much easier to manage your finances whether it’s receiving payments, paying bills, or simply accessing your money.

Benefits of Using the Wise Multi-Currency Account

There are many benefits to using a Wise Multi-Currency Account. We’ve found it to be very useful for both work and personal finances, especially if you deal with different currencies often.

This is how we use Wise to run our companies with an international team and in our daily life.

Paying Our International Team

Wise is the main tool we use to pay our international team, whether it’s for monthly payroll or freelance projects.

At ExpatDen, we work with people from all over the world. Since our articles are based on real-life experience, we collaborate with writers who actually live in the countries they write about. Some are based in Thailand, Indonesia, Vietnam, Canada, the US, Mexico, Slovenia, New Zealand, and more. So it’s completely normal for us to receive invoices from different parts of the world.

Even though our business bank account is a multi-currency account, we still prefer using Wise for several reasons:

- It’s very convenient. We just prepare a simple Excel file and upload it through Wise’s batch payment feature.

- Our default currency is HKD (our company is registered in Hong Kong), and each team member can choose to receive in their preferred currency, whether that’s USD, CAD, THB, or something else.

- After we upload the file to Wise, we log in to our online bank and fund the transfer.

The whole process takes less than 10 minutes. Most of the time, transfers arrive in 1–2 business days. And if the recipient already has a Wise account, they might receive it within 15 minutes.

The only downside is that if the recipient doesn’t have a Wise account, they’ll need to enter their bank details manually via an email link. So we usually give them a heads-up, because if they miss the deadline, Wise will cancel the transfer and we’ll have to resend it.

Send Money Internationally with Low Fees

Whenever we need to send money internationally, whether it’s to pay for services, make business payments, or just send money to family. We use Wise because of its low fees.

This feature is especially useful if you live abroad. For example, you can send money from your home country’s bank account to the country you’re living in. The fee is generally around 1%, which is much cheaper than using a traditional bank, where fees often range from 3% to 4%.

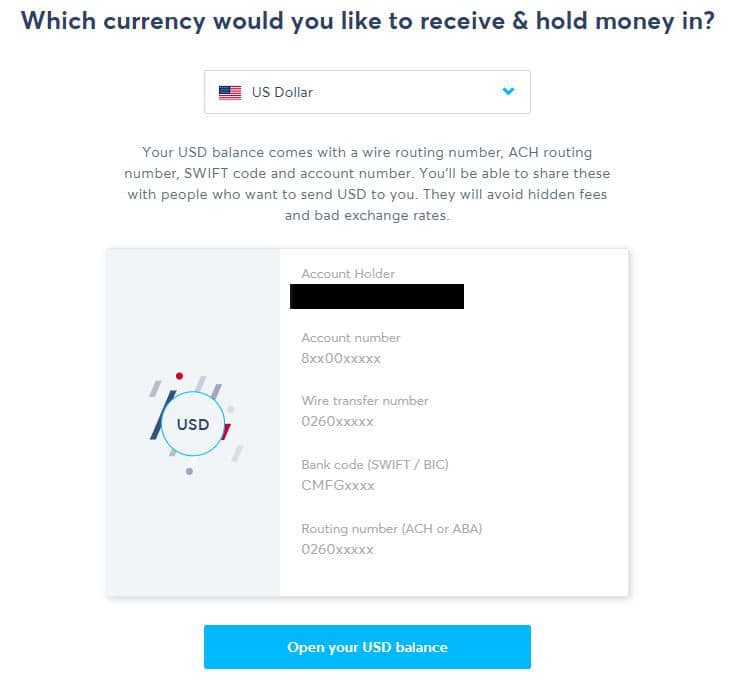

Receive Money in Different Currencies

This is one of the most unique benefits of using Wise, and something you don’t easily get with other providers. Right now, you can receive money in over 40 currencies, including GBP, EUR, USD, AUD, NZD, SGD, CAD, RON, HUF, and TRY. And Wise keeps adding more every year.

When we first opened our Wise account years ago, it only supported around five currencies. But the list keeps growing, which makes it even more useful over time.

This feature can save you a lot on international transfer fees. It’s like having a local bank account in over 40 countries. Your client or customer can pay you with a local transfer, and then you convert the currency within Wise and withdraw it to your own bank account.

For example, if you’re an American working with a European client, you can ask them to pay you in EUR through your Wise account. Then, you just convert it to USD inside Wise and withdraw it to your U.S. bank. The conversion fee is usually only around 0.5%.

If they had sent the payment directly to your U.S. bank, you’d probably pay a fixed international transfer fee (often around US$50) plus a hidden exchange rate fee of about 1%. So the savings really add up.

You can also receive payments from platforms like Amazon, PayPal, and Stripe directly into your Wise Multi-Currency Account.

Tip: I usually set a Wise exchange rate alert and only convert when the rate is favorable. It’s an easy way to get more value from your money without doing anything extra.

Real-Life Examples

I also have another travel company in Japan. Once, a customer from Singapore wanted to pay in SGD. So we just opened a SGD balance in Wise, sent them the local bank details, and after the payment came in, we converted it to JPY and withdrew it.

Another friend, who’s a freelancer, uses Wise to get paid by U.S.-based freelancing sites. Many of those sites require a U.S. bank account. And Wise makes that possible.

Pay Locally

One of the main challenges expats face when moving to a new country is that they can’t open a local bank account right away. But when it comes to renting a place, most landlords want to be paid via local bank transfer.

Of course, it’s possible to pay using your home country bank account — but there are two major issues:

- high international transfer fees

- difficulty tracking the payment

I’ve received questions from readers about this problem. Recently, one of our German readers living in Thailand told me he had this exact issue. He paid his Thai landlord from his German bank account. The money was deducted, but the landlord never received it.

Unfortunately, this turned into a dispute. The landlord even considered canceling the rental contract and keeping the deposit, claiming he was never paid, even though the payment was made. The issue may have been caused by a mismatch between English and Thai names on the transfer.

I checked with a lawyer in Thailand, and he confirmed that this kind of problem is very common.

But with Wise, it’s easier to prevent these misunderstandings. You can share payment proof via email directly from your Wise account. Or use the batch payment feature and let the recipient enter their own bank details to make sure the money goes to the right place.

Once you open a Multi-Currency Account, you can also request a Wise debit card. It works just like any regular debit card. You can use it to pay at shops, withdraw from ATMs, or shop online, anywhere in the world.

Withdraw Cash

With the Wise debit card, you can withdraw money from ATMs globally, as long as they support MasterCard. The fees are usually lower than what traditional banks charge.

This means you don’t need a local bank account just to access cash. But if you’re planning to stay long-term (a year or more), it’s still a good idea to open one eventually.

Just keep in mind that ATM fees still apply. Depending on the country, they’re typically around US$5–US$10 per withdrawal.

How the Multi Currency Account works

When you activate a multi currency account, you will get bank address details for receiving both local and international transfers.

- You’ll be able to receive money from family, friends, companies, and clients.

- You can also use it to send money in over fifty currencies that are supported by Wise.

One important thing to understand is that the Multi Currency Account is not an actual bank account. Instead, it is a virtual account that has many, but not all, the features of a real bank account.

For example, the Multi Currency Account DOES NOT ACCEPT

- Cash

- Checks

- Pay interest

It is not covered by any government-run account insurance schemes, like the Federal Deposit Insurance Corporation or the Financial Services Compensation Scheme.

Fees

There are three main fees when using a Wise Multi-Currency Account:

- wire transfer fees

- currency conversion fees

- withdrawal fees

- bank fees

While these fees do exist, Wise still ends up being cheaper than most traditional banks, mainly because the transfer and conversion fees are much lower.

Another big plus is transparency. Unlike many banks, Wise shows you exactly how much you’ll pay before you make a transaction. No hidden charges, no surprises.

As a plus, since you control when you want to convert, you get more money when rates are good.

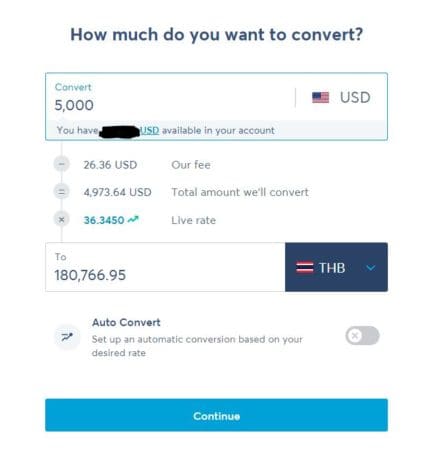

Currency Conversion Fees

Wise is known for its cheap currency conversion fees, which are reflected in its Multi-Currency Account.

Wise uses the mid‑market rate and charges a transparent fee that typically ranges from 0.33 % to around 2 %, depending on the currency and amount. For popular corridors like USD, EUR, CAD, and NZD, the fee is usually around 0.4 %.

Compared to traditional banks, Wise’s exchange rates can save you around 5 % to 6 % on USD conversions. Below is the revised comparison table (based on current mid‑market vs. typical bank rate):

| Currency | Mid-Market (Wise) | Typical Bank Rate (estimate) | Difference vs Mid-Market |

|---|---|---|---|

| EUR | 0.8444 EUR | ~0.82 EUR | ~3.0 % |

| GBP | 0.7378 GBP | ~0.72 GBP | ~2.3 % |

| AUD | 1.4145 AUD | ~1.37 AUD | ~3.1 % |

| NZD | 1.6669 NZD | ~1.61 NZD | ~3.3 % |

| CNY | 6.9088 CNY | ~6.65 CNY | ~3.7 % |

| CAD | 1.3646 CAD | ~1.32 CAD | ~3.2 % |

*Rate as of February 18, 2026

Wire Transfer Fees

When someone sends money to your Multi-Currency Account, Wise charges you a small fixed fee of US$6.11 This is lower than traditional banks. For example, major U.S. banks often charge between US$15 to US$30 when receiving money from abroad.

Withdrawal Fees

When you use your Wise Multi-Currency Account to send money to your bank, Wise charges another small fixed fee of US$0.5 to US$1.

Bank Fees

This only applies when you use Wise to send money to someone else. To do that, you usually pay Wise from your local bank account. And this may involve a small local transfer fee. For example, for our company in Hong Kong, the local bank charges around HKD 10 per transfer (about US$1.27).

Total Fee

From our experience of sending money to major currencies many times, the total cost, including all fees (transfer, conversion, local bank), is usually around 1% of the transaction amount. That’s very cheap. In some cases, it’s even lower than the rate you’d get from exchanging cash at a money kiosk, and a lot more convenient and secure.

Transfer Speeds

We’ve been using Wise for many years to send money to people around the world.

- In most cases, the money arrives within a day after we make the transfer.

- If the recipient already has a Wise account, the transfer can be completed in under an hour.

The only delay we’ve run into happens when using batch payments and the recipient doesn’t enter their bank details in time. If that happens, the transfer gets held up or canceled, and we have to resend it.

Safety and Security

After years of using Wise, we’ve never had any security issues. We’ve made hundreds of transactions, and everything has gone smoothly. Our account has never been breached.

Whenever you log in from a new device, Wise requires two-step authentication, which adds an extra layer of protection.

The only issue we’ve come across was when one of our editors got logged out of his account a few years ago. He couldn’t access it for a while and had to go through the full verification process again.

If you’re looking for more details about Wise’s official regulations, keep reading below.

Wise is a UK-based firm, registered as an Electronic Money Institution (EMI) by the Financial Conduct Authority (FCA). As part of this regulation, Wise is required to keep customer funds in segregated accounts, completely separate from its own operating funds. This means that in the unlikely event of Wise becoming insolvent, customers’ funds are protected and would be reimbursed.

Because Wise is regulated under the UK’s Electronic Money Regulations, it’s held to the same high standards of financial conduct as other major financial institutions in the UK, a country known for its strong and trustworthy financial system.

In the United States, Wise US Inc. is registered with FinCEN as a Money Services Business and is licensed as a money transmitter in nearly every state. This ensures Wise complies with strict anti-money laundering laws and financial regulations.

It’s important to note that Wise is not a bank, so customer funds in the U.S. are not FDIC-insured by default.

However, Wise holds those funds in safeguarded accounts at FDIC-insured banks or in secure liquid assets, which adds an extra layer of protection. If you opt in to Wise’s interest feature, some of your balance may also qualify for FDIC insurance, up to the standard coverage limits.

Bottom line: Wise is a highly regulated and transparent financial service provider. Whether you’re sending small personal transfers or large international business payments, Wise is a safe and reliable platform to use.

Ease of Use

The Wise Multi-Currency Account is very easy to use. I downloaded an app on my phone, and it works much like a regular banking app. Once you log in, you can quickly see how much money you have in each currency, including the balance on your debit card.

You can send money in just a few clicks and even save payment details for your favorite contacts to make future transfers faster.

The only minor issue I’ve had was the first time I used the batch payment feature in my computer. It requires uploading a CSV file with data in the exact format specified by Wise. So it took a bit of trial and error to get it right.

How to Open a Multi Currency Account

It is easy to open a Multi Currency Account.

Open a Wise Account

You must first sign up with Wise. You’ll have to decide whether you want to use your account for personal or business purposes. Other than that, the sign-up process for Wise is extremely easy.

Here’s how to open a Wise account:

- Enter your email address and create a password

- Verify your identity (usually with a passport or national ID)

- Link your local bank account or debit/credit card for funding.

Open a Currency Account

Once your main Wise account has been set up, you must go to the Balances tab if you’re using a computer or the Account tab if you’re using the Wise mobile app.

Then you simply need to select in which currencies you would like to keep your balance.

You can also add money to your balances in any currency at any time by simply clicking the Add button and selecting which of your bank accounts you’d like to send the money from.

Additionally, for British pounds, Australian dollars, New Zealand dollars, U.S. dollars, and euros, you will receive account numbers, including SWIFT codes and IBANs.

You can also readily convert money from one currency to the other between your existing balances, getting the real exchange rate and being charged one of the lowest conversion fees in the business.

Get A Wise Card

At this point, you will also be able to sign up for a Wise Card, which will allow you to withdraw your funds from virtually any ATM machine in the world while also being able to pay anywhere MasterCard is accepted.

Wise Card

Once you have a Wise Multi-Currency Account, you can apply for the Wise Card for a one-time fee of US$9. You’ll get both a physical card and a digital card, which you can add to Apple Pay or Google Pay for contactless payments.

The Wise Card works just like a normal debit card. For me, there are two main uses:

- Locking in a currency in advance when traveling. For example, if I’m planning a trip to Japan, I’ll exchange JPY in my Wise account ahead of time when the rate is good — then use that balance while in Japan.

- Emergency ATM withdrawals. You get two free ATM withdrawals per month, with a combined limit of US$100. After that, Wise charges a small fee.*

*Note: Wise’s ATM withdrawal policy changes from time to time. In the past, the monthly free limit used to be US$250, so it’s good to double-check their current terms before you travel.

The Wise Card is a great backup to have, especially when you’ve just moved to a new country and don’t have a local bank account yet. But if you plan to live there long term, I personally think having a local bank account is more convenient for daily use.

One downside: The Wise Card is only available in selected countries. This includes Australia, Brazil, Canada, Switzerland, Japan, Malaysia, New Zealand, the Philippines, and Singapore. If your country isn’t on the list, you won’t be able to apply for the card just yet. There’s also some countries where the card won’t work. See a full list here.

Community sentiment in 2026 aligns with our experience: Wise remains the default recommendation in expat and digital nomad groups for multi-currency accounts, largely because no competitor has matched its combination of transparency, exchange rates, and ease of international transfers. The most common complaint is temporary account holds during identity verification, which can freeze access for days if you haven’t uploaded all your documents upfront.

What I Don’t Like about Wise

While Wise is a great tool for international payments and currency management, it does come with a few limitations. Whether these are real drawbacks depends on what you’re looking for.

There are two main drawbacks:

Can’t Replace a Traditional Bank

If you’re planning to use Wise as a traditional bank, you may want to think twice. Wise still can’t fully replace a traditional bank. It’s not just about missing services like loans or credit cards, it’s about core functions.

While nothing beats Wise for international transfers, local transfers are still cheaper and more convenient through a local bank. For example, in Thailand, cashless payments are widely accepted. You can pay for many things just by using your bank app to scan a QR code.

Not Available in Every Country

While it’s clear that Wise is doing its best to expand globally, its functions are still limited in certain countries. For example, you still can’t use Wise to send money from Thailand or China.

The Wise multi-currency card also isn’t available in Hong Kong.

This mostly comes down to financial regulations in those countries, so it’s unlikely to change anytime soon.

The good news is that if you’re from countries like the UK, USA, Canada, Australia, or most of Europe, you can access the full range of Wise’s features.

Should You Open a Wise Multi-Currency Account?

In my opinion, here’s the type of person who should open a Wise Multi-Currency Account:

- If you’re a traveler or digital nomad who goes abroad regularly. While the Wise card isn’t perfect, it still works well.

- If you live abroad and need to send money from your home country regularly, whether it’s a pension or any other type of income.

- If you have clients abroad. A Multi-Currency Account can save you a lot on exchange rates and transfer fees.

- If you need to send money abroad regularly, whether to a service provider or your international team. Wise fees are among the lowest in the market.

To put it simply, if you regularly deal with currency conversion, it’s a good idea to open a Wise Multi-Currency Account. You can use this link to open an account for free.

On the other hand, if you mostly stay in a single country and don’t need to make international transfers, you probably don’t need it.

Additional Tips to Get the Most Out of Your Wise Multi-Currency Account

Here are some personal tips to help you maximize your Wise experience:

- Open your account early. Sometimes Wise may ask for proof of address during the account opening process, which can be hard to provide if you’ve just moved to a new country. It’s easier to get verified while you still have access to documents from your home country.

- Set a rate alert. You can ask Wise to notify you when your preferred exchange rate is reached, or even set it to automatically convert money once the rate hits your target. This helps you avoid poor exchange rates when transferring large amounts.

Alternative Services

There are many services that overlap with the features offered by Wise. However, when it comes to sending money from one bank account holder to another in a different country, Wise is almost always the cheapest, easiest-to-use, and fastest option.

The closest alternative to Wise would be Revolut. Both services offer multi-currency accounts and international transfers, but they have different strengths:

- Wise is better for sending money abroad.

- Revolut offers more tools like budgeting features, crypto trading, and travel perks. It also supports more lifestyle-related services, especially in Europe and the UK. However, its international transfer fees tend to be higher than Wise.

To put it simply, if your main goal is to find a reliable tool to send or receive money abroad, Wise still wins for me.

FAQs about Wise Multi-Currency Account

Is Wise a real bank?

No. While Wise is an authorized financial institution, it’s not a traditional bank. It offers many bank-like features such as holding balances, international transfers, and a debit card. However, it doesn’t offer services like loans, credit cards, or insurance. You also won’t earn interest by leaving your money there.

Can I open a Wise Multi-Currency Account if I just moved abroad?

While it’s possible, it’s best to open the account before you move. Wise may ask for proof of address in your current country, which can be hard to provide if you’ve just relocated. Verification is usually easier while you still have access to documents from your home country.

How long do Wise transfers take?

Based on our experience, transfers usually arrive within 1–2 days after you fund the payment to Wise. If the recipient already has a Wise account, the transfer can take just a few hours or even less.

What currencies can I hold in my Wise account?

You can hold and convert over 40 currencies, including USD, EUR, GBP, AUD, JPY, SGD, and more. Wise continues to add new currencies every year. (When we first signed up, it only supported five.)

Can I use Wise to receive payments from clients or platforms like PayPal or Amazon?

Yes. You get local bank details (e.g., USD, EUR, GBP) to receive payments just like a local. Platforms like Amazon and Stripe work well with Wise. PayPal may allow it in some regions, but you should double-check compatibility first.

Is it free to open the Multi-Currency Account?

Yes. There are no signup, monthly, or recurring fees for opening and holding a Multi-Currency Account. You only pay fees related to specific transactions, such as currency conversion or transfers.

Is the Wise Card available in my country?

The Wise card is currently available in selected countries like the UK, EU, Australia, New Zealand, Japan, Singapore, Malaysia, Canada, Brazil, and the Philippines. If you live outside these regions, you may not be able to order the card yet.

Can I withdraw cash from ATMs with Wise?

Yes. You can use the Wise debit card to withdraw cash from ATMs worldwide. The first two withdrawals per month (up to a combined US$100) are free. After that, a small fee applies. Be sure to check the current terms, as they may change.

Can I use Wise for business purposes?

Yes. And that’s exactly what we use it for. Wise is our main tool for paying our international team and clients. It’s fast, reliable, and much cheaper than traditional banks.